Before starting to invest in the financial markets, any investor should have a good understanding of the basics of finance. Here they are :

- The value of money over time

- The relationship between risk and return

- Diversification

We will explain each of these bases in detail in the following pages.

1) The value of money over time:

The central principle of investing is that a dollar today is worth more than a dollar tomorrow.

- Inflation erodes purchasing power over time.

- Savings can be invested and grow with the return obtained.

How do you calculate the value of money over time?

There is capitalization (future value of today’s $) and discounting (today’s value of future.

- Simple interest capitalization: this is the interest paid on your initial savings.

PV × (1+ Int) = FV where Present Value (PV), Interest (Int), Future Value (VF)

Example: I invest $ 100 today at a rate of 5%. A year later, my investment will be worth 105$ [100 × (1.05) = 105]

- Compound interest capitalization: this is the interest paid on your initial savings plus the interest on the interest received so far. Thus, the amount to which the interest rate is applied will increase more and more rapidly over time. In other words, the growth of savings will be exponential, hence the phrase: the magic of compound interest.

PV × (1+ Int1) × (1+ Int2) = FV

- Example: I invest $ 100 today at a rate of 5%. Two years later, my investment is worth 110.25$ [100× (1.05) × (1.05) = 110.25]

- Discounting: the reverse of capitalization Example: how much should I invest to get $ 105 in 1 year at 5% interest rate. 100$ [105÷ (1.05) = 100]

We will use the capitalization to determine when you will have accumulated the necessary sum to complete a project that is important to you (for example the down payment for the purchase of a house).

Discounting will allow us to know how much to save in each pay period to achieve the desired standard of living on your chosen retirement date.

2) The relationship between risk and return:

The riskier (and more volatile) an investment is, the higher the expected return will be. An investor will be willing to tolerate some volatility in exchange for a higher expectation of profit.

So generally:

- A bond with a long maturity will be riskier than a short one.

- A corporate bond will be riskier than one of its Government with the same maturity.

- A corporate bond will be less risky than its stock.

- A share of a small company (capitalization) will be riskier than a large company.

- Etc.

3) Diversification :

Like the magic of compound interest, diversification brings huge benefits to a portfolio.

Diversification is an effective way to reduce the risk of a portfolio without reducing the potential for returns. Indeed, diversification makes it possible to build a portfolio whose total risk is lower than the combined risks of individual securities.

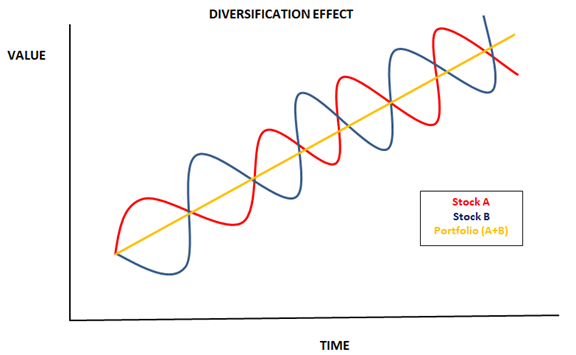

How is that possible? Here is a stylized example.

In the following graph, there are 3 investments, A share, B share and a portfolio made up of these 2 securities. We can see that the A and B shares are trending upwards, but with some volatility. It is also noted that their progressions do not occur at the same time (concept of correlation). However, by combining 2 volatile securities, but whose evolution is the opposite, we manage to create a portfolio (A + B) in constant progression (without volatility).

The correlation between two financial assets is the strength of the link that exists between these two variables. A strong positive relationship will have a correlation of +1 while a strong negative relationship will have a -1.

In reality, diversification is not as perfect as in this example, but it is still beneficial and necessary.

The most obvious example is that the yield on bonds often moves in the opposite direction to that of stocks.

Diversification is one of the rare free strategies, so you have to take advantage of it.

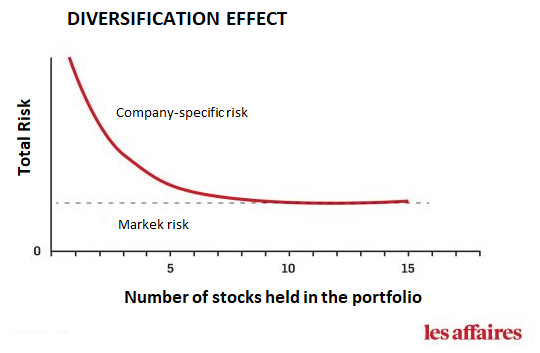

Diversification is usually achieved by adding only a few securities or asset class, as shown in the following chart.

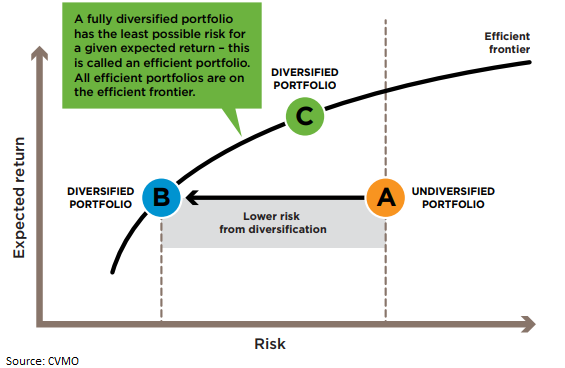

When a portfolio is fully diversified, it will be said to be optimal. Therefore, an investor will have to take additional risks to increase his expected return. This is the return of the notion of return and risk.

In the following graph, portfolio A is undiversified while portfolio B is diversified and optimal. Compared to portfolio B, portfolio A has the same return but a higher risk. As for portfolio C, it is also efficient but at a higher level of risk (and return).

Now that we know the basics of finance, we can use these concepts to deepen and broaden our knowledge of investing.

In the next chronicle, we will analyze the asset class of Fixed Income Assets.

Frédéric Mercier CFA, SIPC

Director – Financial markets