A well-diversified portfolio generally consists of fixed income assets and securities (stocks).

A fixed income asset is the equivalent of a loan made by an investor to an issuer. In return, the issuer undertakes to pay the interest provided for in the contract and to repay the capital on the due date.

What are the main fixed income markets?

Money market: consists of investments with a maturity of less than one year. Here are the main products:

- Treasury bills: they are issued by the federal government and the provinces.

- Commercial paper: short-term unsecured debt security issued by a company.

- Bankers’ acceptances: debt securities issued by companies whose repayment is guaranteed by a bank.

Bond market: consists of investments with a maturity of more than one year. Here are the main products:

- Government bonds: Federal, provincial, municipal

- Corporate bonds

What is the role of fixed income assets in a portfolio?

- They provide stability and diversification to the portfolio, as they are less volatile than equities (stocks).

- They provide predictable income because the coupon (interest income) is known in advance.

- They provide a source of liquidity to the portfolio.

The relationship between interest rates and the price of fixed income assets

As the name suggests, interest income is known in advance and is stated in a contract (for example, an interest rate of 4% per annum).

How do you calculate the price of a bond?

To do this, we need to resort to the concept of discounting that we saw in the chronicle on the basics of investing.

This involves updating the coupons to be received at different periods and the capital at maturity.

Where Price = P, cpnn = Coupon for period n, i = Interest rate, CN = Capital, ∑ = Sum, N = Period remaining until maturity, tn = time remaining until receipt of the cashflow.

In short, we bring back all cash flows receivable as of today. Coupons are known, but the rate fluctuates in the market according to investors’ expectations and risk appetite.

Let’s look at some examples:

A new 5-year bond is issued by the Government of Canada.

The current market interest rate for this term is currently 2%.

The coupon of this new bond will be set at 2%. An investor will lend $ 100 today in exchange for 5 annual payments of $ 2 and $ 100 in 5 years. It will achieve a return of 2%.

For example, the rate of inflation continues to rise, causing investors to now charge 2.5% interest for that term. The $ 2 coupons have already been set. If a new investor wants a 2.5% return, the price must necessarily go down for them to be interested in this bond. Technically, the investor will discount the fixed cash flows at 2.5% instead of 2%.

This investor will lend $ 97.68 today for 5 annual payments of $ 2 and $ 100 in 5 years. It will achieve a return of 2.5%.

Now the recession is on the horizon and the Bank of Canada is expected to start lowering its key rate. Investors now charge 1.5% interest for this term. The $ 2 coupons have already been set. If a new investor wants to get 1.5% return, the price must necessarily go up, because the demand for this bond (with higher coupons) will be greater. Technically, the investor will discount the fixed cash flows at 1.5% instead of 2%.

This investor will lend $ 102.39 today for 5 annual payments of $ 2 and $ 100 in 5 years. It will achieve a return of 1.5%.

The preceding examples clearly show us that the price of bonds is inversely related to movements in interest rates.

What are the factors that influence fixed income assets?

- The risk-free rate is the central bank’s key rate.

- The fluctuation of interest rates varies with economic conditions.

- Instruments with a longer maturity generally offer a higher yield than instruments with a shorter maturity.

- The interest rate curve is a graphical representation of an issuer’s market rates of return according to their maturity. However, rate variations are not identical on the curve, depending on monetary policy, inflation, etc.

- The credit quality of the issuer. The lower the financial strength of the issuer, the more investors demand high interest rates.

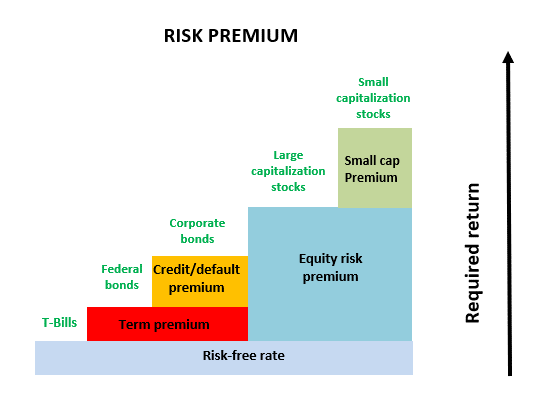

The risk-return relationship of fixed income assets

Let us return to the concept of risk and return. The more risky (and volatile) an investment, the higher the required return will be. An investor will be willing to tolerate some volatility in exchange for a higher expectation of profit.

The return on an asset can be represented as a combination of risk premiums. The following graph is a summary representation of the risk premiums for various investments.

Let’s look at an example of a corporate bond (as of Nov 16, 2021):

A 5-year bond from Bell Canada.

Risk-free rate (3-month Canada Treasury bills) = 0.12%

5-year Government of Canada Bonds = 1.51% (1.39% maturity premium)

Bell Canada 5 year bond = 2.82% (1.31% credit premium)

So, the current rate of return on a 5-year Bell Canada bond is made up of 3 premiums:

Risk-free rate of 0.12% + maturity premium of 1.39% + credit premium of 1.31% = 2.82%

These premiums fluctuate over time and have their own dynamics.

In the next chronicle, we will continue to deepen the concept of risk premium and analyze the Equity assets class.

Frédéric Mercier CFA, SIPC

Director – Financial markets