FINANCIAL MARKETS REVIEW

The election of Donald Trump had a significant impact on the stock markets in America. Indeed, Trump’s very business-oriented vision has instilled a marked optimism in the stock markets. The S&P 500 index rose by 5.9%, while the TSX index’s performance was 6.4%. In the United States, all sectors ended the month up. The most significant increases were in the consumer discretionary and financial sectors. In Canada, the main gains came from technology and financials.

Elsewhere in the world, stock markets were flat or slightly negative, as in emerging markets.

Although very volatile during the month, interest rates ended virtually at the same level as at the end of October. 10-year yields ended down 0.10%, generating a performance of 1.28% for the Canadian bond index.

OUTLOOK:

Economy:

The gradual decline in interest rates, combined with low equity market volatility, is leading to an improvement in US financial conditions. Simply put, financial conditions represent the cost and ease of obtaining financing (debt and equity) for a company. It is therefore not surprising to see that an improvement in financial conditions is reflected in GDP growth. This bodes well for 2025 in the United States.

Financial conditions and GDP (United States):

A few indicators have come out of their torpor recently.

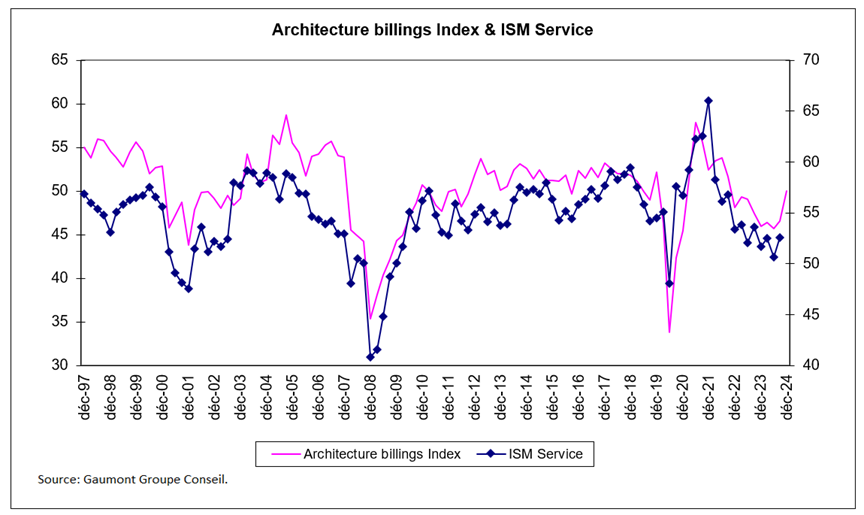

First, the Architects Activity Index is a good indicator of the service sector. After 20 months in contraction mode, activity growth has returned to growth mode. One month does not make a trend, but it is still positive for the economy.

Architects Activity Index and ISM Service (United States):

Then, the Philadelphia Federal Reserve Future New Orders Index. This indicator has been gradually increasing for several months and almost reached a historic record in November. This indicator informs us of the trend of new manufacturing orders in the United States, but 6 months in advance.

Philly FED Expected New Orders and ISM New Orders (United States)

The signals are therefore good for the 2 major blocks of the economy, namely the manufacturing sector and the services sector.

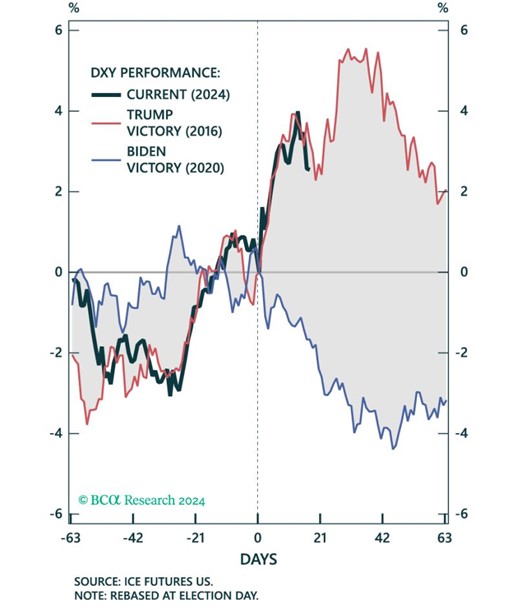

The Canadian Dollar and the Euro have lost feathers since the election of Donald Trump. The evolution of currencies (against the US dollar) is almost identical to that of 2016. The worst is probably behind us.

Evolution of the US Dollar (vs a basket of currencies) during Trump’s victories

Fixed Income:

Milton Friedman said that « inflation is always and everywhere a monetary phenomenon. It can only be generated by an increase in the quantity of money faster than the increase in production ».

However, since the pandemic, we can see that Friedman was not wrong. In the following graph, we can see that inflationary pressures are expected to continue to decline in the first half of 2025 and stabilize thereafter.

Inflation and the money supply (United States):

Central banks will therefore be able to continue to lower their key rates. To this end, nearly ¾ of central banks are currently in easing mode.

Key rate cuts around the world:

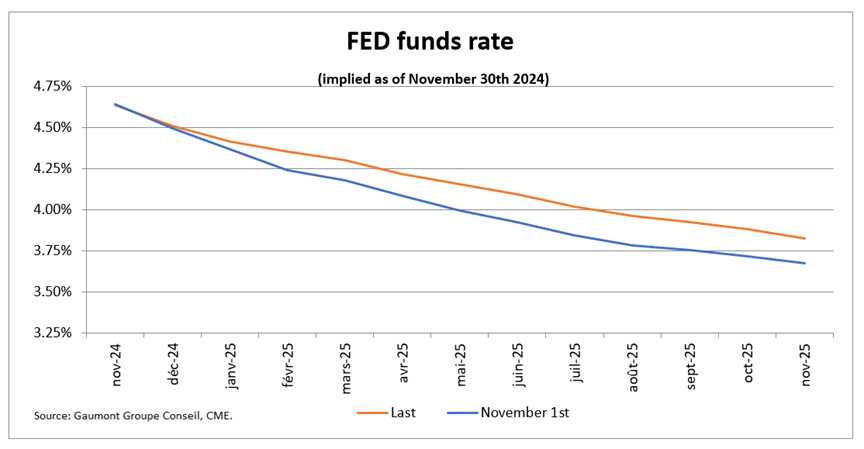

The Fed will continue to cut rates in order to lower real rates. Over the next 12 months, the Fed is expected to cut rates by 1.04% (market participants’ expectations). The Bank of Canada and the Fed are both expected to cut rates by 0.25% in December.

Short-term Implied Interest Rates (US):

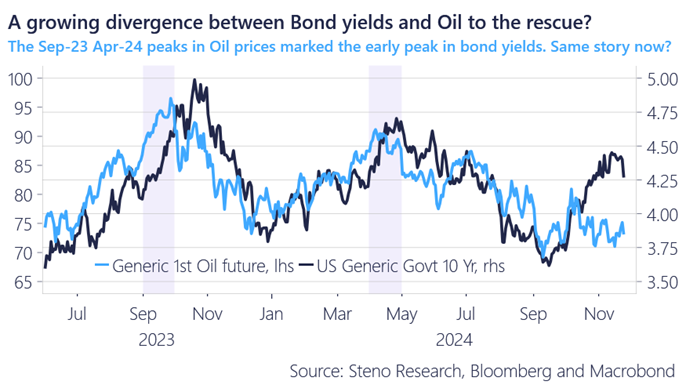

The decline in short-term rates will continue to put downward pressure on longer-term rates. In addition, the weakness in the price of oil (which is closely linked to inflation) will maintain downward pressure on 10-year yields.

10-year interest rates and crude oil prices (US):

Stock Markets:

The savvy stock market investor must:

• Understand the fundamental assumptions that are reflected in the price of a stock.

• Manage your emotions to avoid buying in euphoria and selling in panic.

We have already discussed the price-earnings ratio. This indicator continues to hover near historic highs in the United States. There are others. Indeed, there are profit margins that influence profit growth. In the following graph, we see that the expected margins, as well as profit growth, are very optimistic. The risk of disappointment is high.

Fundamental data on the S&P 500 index:

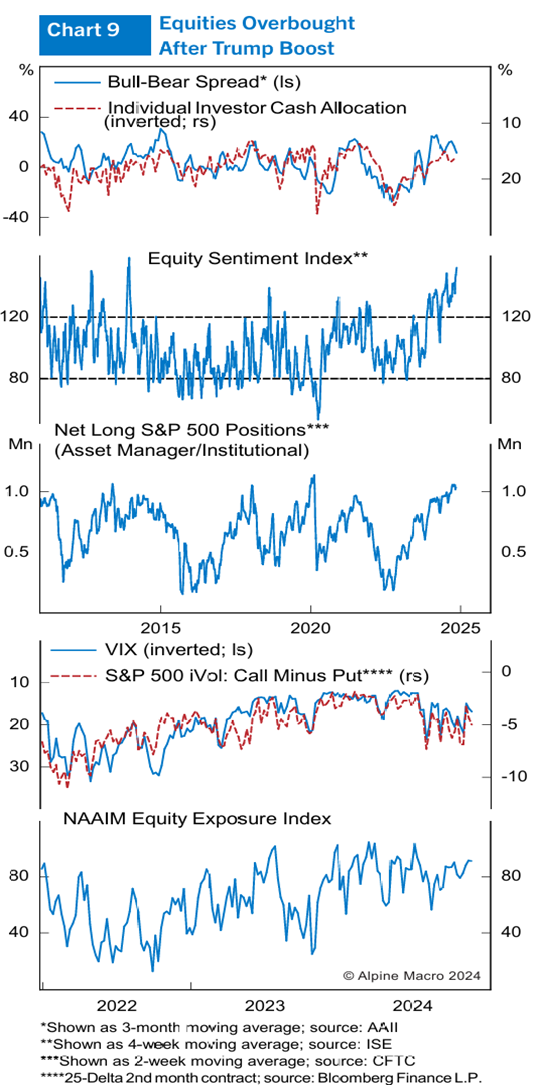

As for the sentiment of market operators, there is also a panoply of them. Periods of euphoria are noted when the markets have already progressed a lot and some investors become more aggressive in their positions, via leverage for example. This pushes the markets up, but at a certain point their ammunition is exhausted. It therefore does not take a shock or bad news for them to start selling aggressively and push the market down.

In the following graph, we see that the various indicators point to a feeling of euphoria among investors. The reversals are generally more severe when such a level of optimism prevails.

Sentiment data on the S&P 500 index:

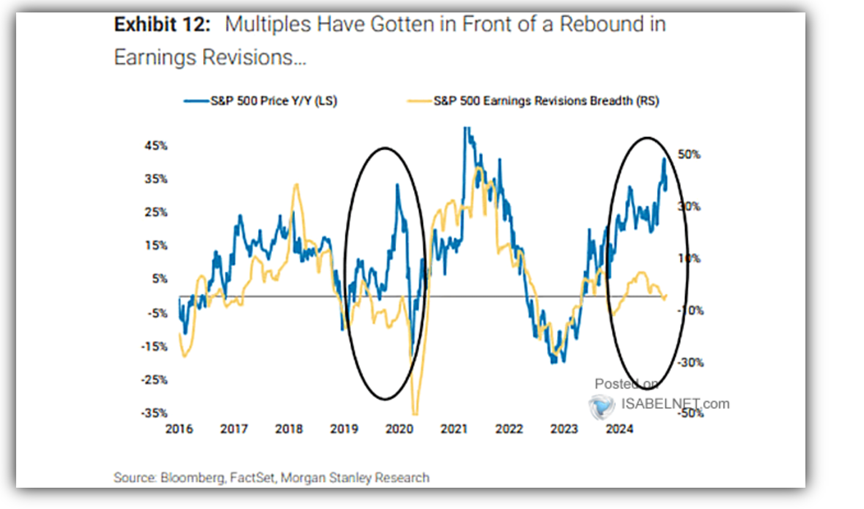

Finally, a last graph that combines the two concepts illustrated previously. Generally, upward revisions of corporate profits go hand in hand with the progression of stocks. We note, not only that there is a big divergence between the progression of prices and earnings revisions (Euphoria), but also the absolute level of revisions which is slightly negative (negative fundamental).

Revision of the profit and growth prospects of the S&P 500 (United States):

CONCLUSION :

Bonds remain attractive in terms of return/risk. The global economy continues to improve, although divergences remain. Market volatility provides an opportunity to acquire quality securities with reasonable valuations.

Frédéric Mercier CFA, SIPC

Director – Financial markets