FINANCIAL MARKETS REVIEW

After massively celebrating the election of Donald Trump, stock markets recovered in December. The S&P 500 index fell by 2.4%, while the TSX index returned -3.3%.

Elsewhere in the world, stock markets were slightly positive, including emerging markets (+1.2% return).

The Canadian dollar continued to fall, following the resignation of Finance Minister Chrystia Freeland and the Bank of Canada’s key rate cut of 0.50%. The Fed also lowered its key rate, but only by 0.25%.

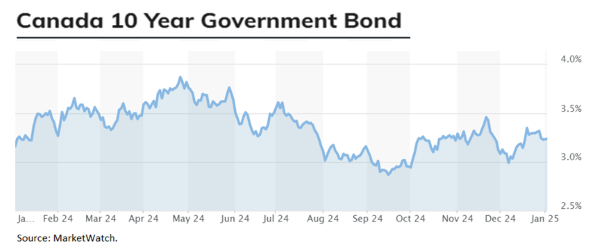

Canadian 10-year yields rose 0.11%, generating a performance of -0.38% for the Canadian bond index.

OUTLOOK:

Economy:

Two months after the election of Donald Trump, we are starting to see its impact on economic and financial data. Its impact on consumer confidence is unequivocal. First of all on small business confidence (NFIB). The jump in confidence in December corresponds to the peak of the last 44 years. Subsequently, at the household level, confidence also exploded. All this is positive for economic growth.

Confidence indices following the election of Trump (United States):

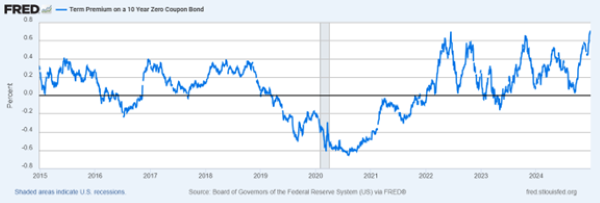

In terms of interest rates, the premium for holding longer-dated bonds, such as 10-year bonds, is back at its highest level in 10 years. Investors are starting to worry about the US deficit (about 6% of GDP). This is good news for investors, but not for the economy.

Holding premium for 10-year bonds (US):

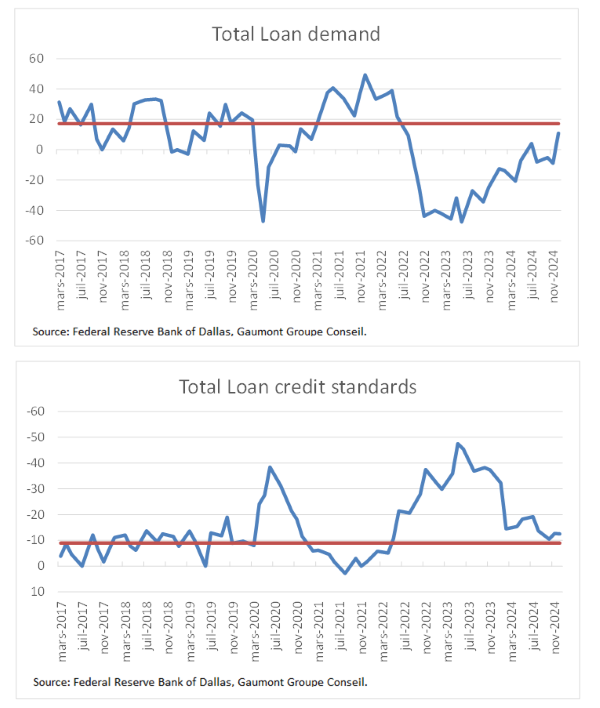

Total loan demand is gradually recovering and is near the pre-pandemic average. Credit conditions remain near their average. This reflects an economy that is regaining strength after the pandemic shock.

Credit conditions and total loan demand (U.S.):

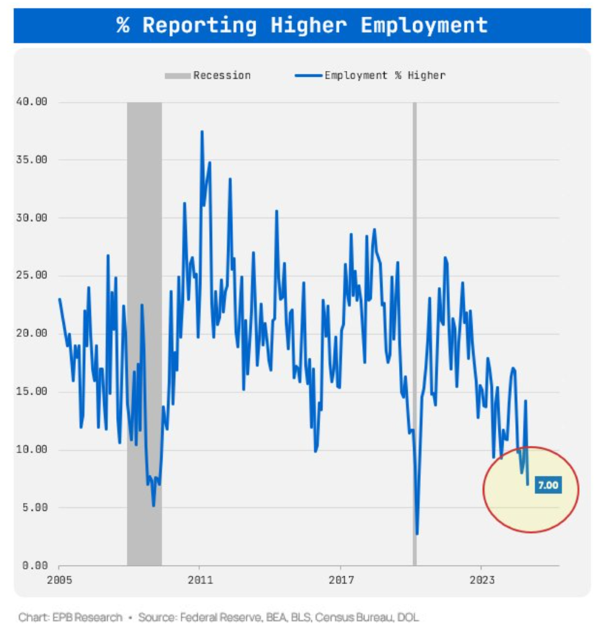

The job market continues to lose feathers. In the latest ISM manufacturing survey, only 7% of industries reported job growth. This is approaching the level of the last 2 recessions. Fortunately, weak employment often comes in the last round of a slowdown or recession.

ISM Employment Index – % of industries growing (United States):

The weakness is most evident in the construction sector. This rebalancing is healthy in an economy that wants to grow sustainably.

Construction Jobs (United States):

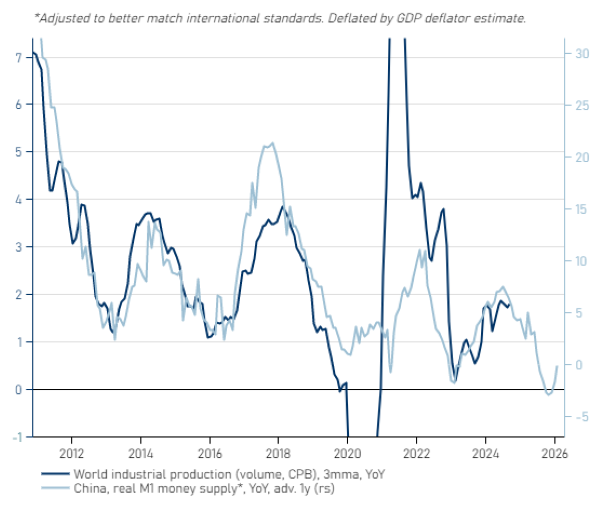

One of the shadows on the picture is the Chinese economy. Their over-indebted economy is on the verge of deflation. Monetary authorities are proactive, but they cannot solve the root causes of the problem. Global industrial production could be under pressure in 2025.

China’s money supply growth and global industrial production:

Fixed Income:

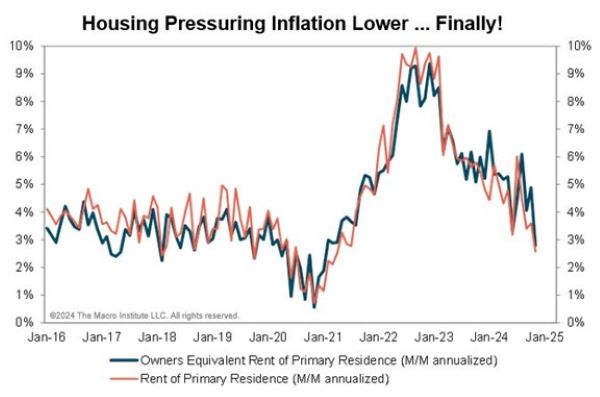

The component of inflation that has kept the price index from returning to normal is the housing component. This component has returned to its pre-pandemic level, as seen in the following chart.

Housing components of inflation (United States):

In addition, the leading indicators of this component inform us that the decline in growth of this component should continue in the coming quarters.

Leading indicator of the CPI housing (United States):

As inflation falls, real interest rates rise! Despite the cuts in the policy rate, monetary policy remains very restrictive. Why keep rates so high when the inflation problem is almost solved. In addition, the strength of the dollar limits inflation of imported products and Trump will not hesitate to put pressure to lower rates.

Monetary policy (United States):

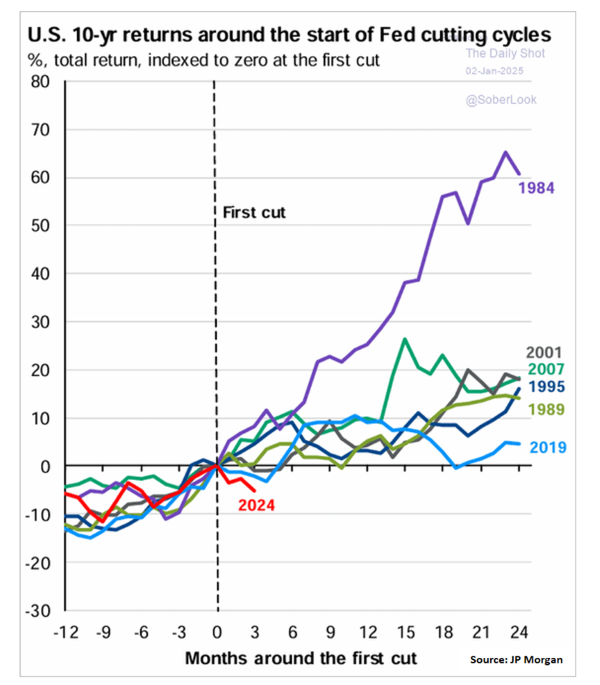

If we look at past cycles of US policy rate cuts, we see that 2024 was the worst year in terms of performance for 10-year bonds. All cycles have their own dynamics, but this is another element that points in the direction that they have risen too sharply.

Bond yields during rate cut cycles (US):

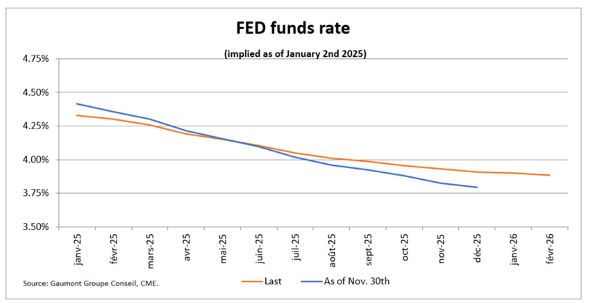

The Fed is now expected to cut rates by 0.50% in 2025. Far from the 1.5% forecast in September. The Fed hates it when the market gets carried away in one direction or the other and does not hesitate to intervene by changing its discourse. It is a safe bet that expectations of rate cuts will increase again in the coming months.

Short-term implied interest rates (United States):

Stock Markets:

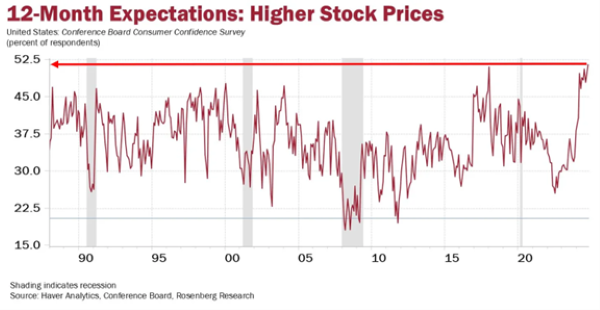

Stock markets corrected a bit in December, but euphoria remains strong. Return expectations are at a 35-year high.

US Equity Market Return Expectations:

The overweight in equities is at its peak and the underweight in cash is also at its peak. There is still some way to go before a balanced market is achieved.

Equity and cash weightings (US):

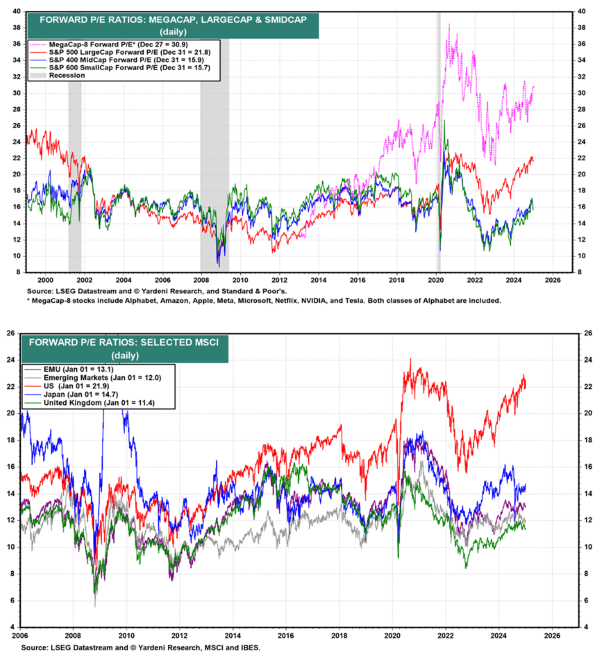

The Mag7s continue to rise (+4.9% in December) but the equally weighted S&P 500 index fell by 6.44%. This index is currently trading at a ratio slightly higher than its historical level. It is now possible to buy large American caps at a reasonable price.

At the end of December, with the exception of the S&P 500 and the Mag7s, the various markets in Europe, Asia and emerging markets are all trading at reasonable valuation levels.

Price / earnings ratio across the world:

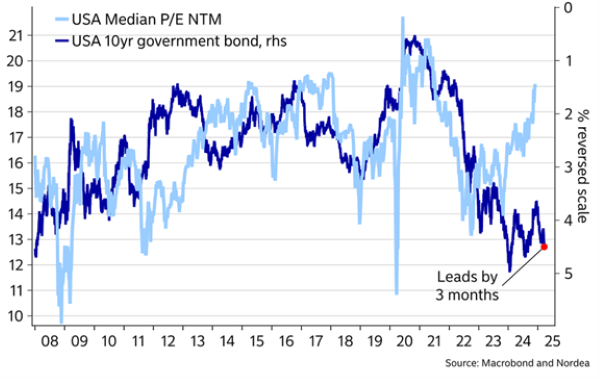

The recent rise in 10-year interest rates means that bonds remain attractive in a portfolio. In the following graph, we can see the close link between interest rates and the price-earnings ratio of stocks. We can also see that a notable divergence remains between these two asset classes. Stocks are expensive at current rates.

Price-earnings ratio of US stocks and 10-year rates:

CONCLUSION :

With the recent rise in interest rates, bonds remain very attractive (especially in the US) in terms of return/risk. However, the stock market (in general) is becoming more and more affordable. The strategy remains to use market volatility to acquire quality securities at a reasonable fundamental valuation.

Frédéric Mercier CFA, SIPC

Director – Financial markets