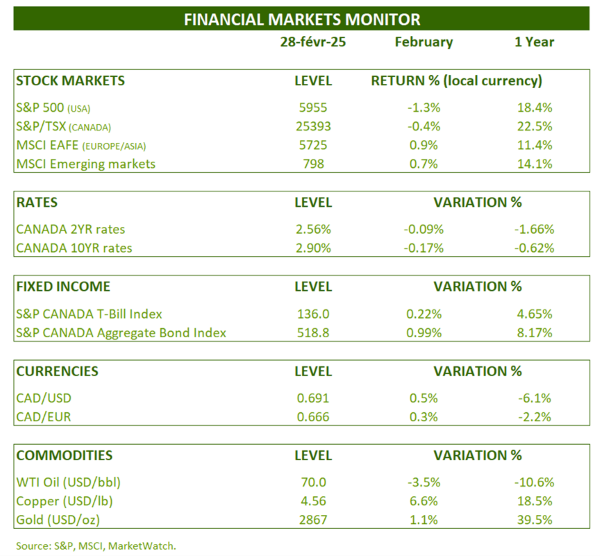

FINANCIAL MARKETS REVIEW

February was characterized by a change in stock market leadership. Stocks (e.g. technology) that were driving the indices up underperformed. Defensive stocks and sectors performed best. We will come back to this.

North American stock markets ended down, while performances were positive in Europe and Asia.

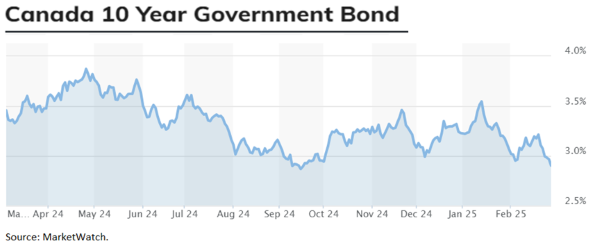

Fears of a global slowdown, caused by President Trump’s tariff threats, are giving global bond markets some breathing room. The decline in 10-year yields has been broad-based across the globe. Canadian 10-year yields fell 0.17%, leading to a strong performance of 0.99% for the Canadian bond index in February, and 2.21% in 2025.

OUTLOOK:

Economy:

Tariffs and DOGE (Elon Musk’s Department of Government Efficiency) were on everyone’s lips in February. Economists conclude that this will result in a modest stagflationary shock. The Apollo investment firm calculated an impact of –0.5% on GDP in 2025 and +0.2% on inflation.

Impact of tariffs and DOGE (United States) government efficiency program:

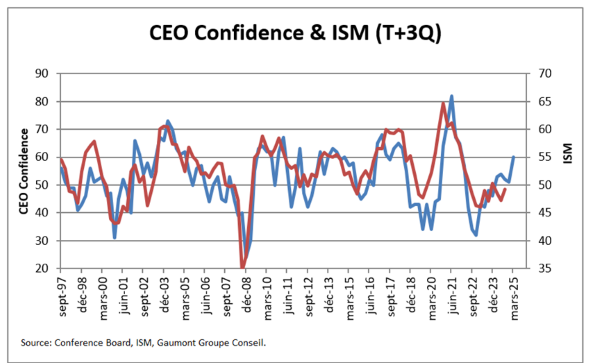

Despite the current uncertainty, CEO confidence has increased significantly recently. This level of confidence is well above the historical average.

Confidence is one of the drivers of the economy. When business leaders are confident, they invest more in the economy and GDP grows faster. In fact, CEO confidence is a leading indicator (by a few quarters) of the ISM, GDP, investment and even the S&P 500. This is encouraging for the future.

CEO Confidence Index (Conference Board) and ISM (United States):

S&P 500 layoff announcements continue to slow rapidly. Elon Musk and his government efficiency department can cut jobs and make headlines, but remember that the private sector accounts for about 90% of jobs in the United States.

S&P 500 Job Losses (U.S.):

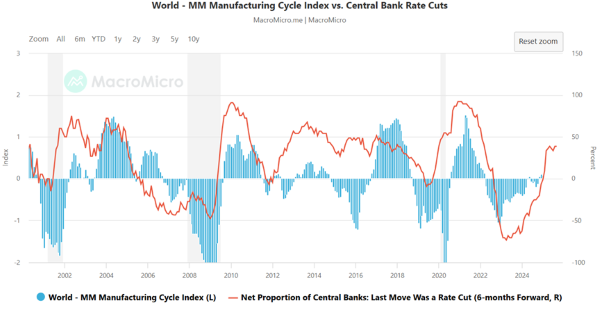

The year 2024 started with a majority of central banks in restrictive mode. Currently, it is quite the opposite, almost 50% are in a phase of rate cuts. Rate cuts take some time to percolate into the real economy. With all these rate cuts, it is permissible to be optimistic about the manufacturing production cycle.

Proportion of central banks in easing mode and global manufacturing index:

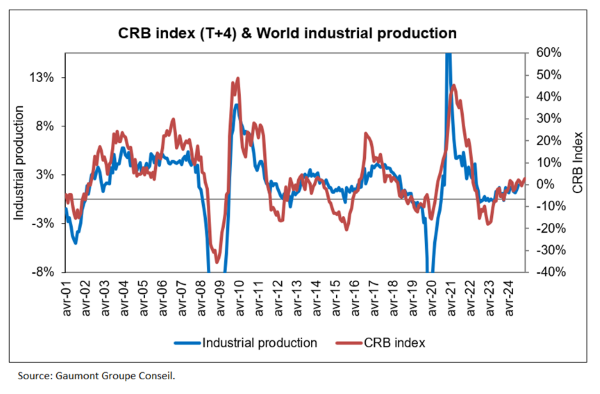

Industrial commodity prices are a leading indicator of global industrial production. This indicator is moving in the right direction and gives us the same signal as the previous graph.

Industrial commodity price growth and global industrial production:

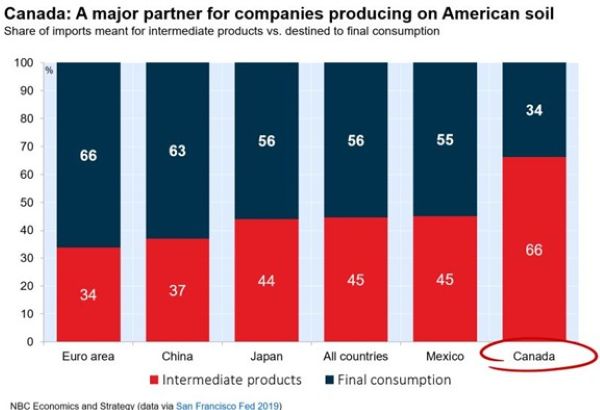

As of this writing, the 25% tariffs on Canadian goods are set to come into effect on March 4. It’s a shame that we’ve come to this, given his economic illogic. Maybe the stock market drop will wake Trump up, possibly. However, in the following graph, we see that 2/3 of American imports are inputs for American companies, which is catastrophic for them. It’s a safe bet that it will be business leaders who convince Trump to remove the generalized tariffs.

Share of American imports destined for intermediate and consumer products:

Fixed Income:

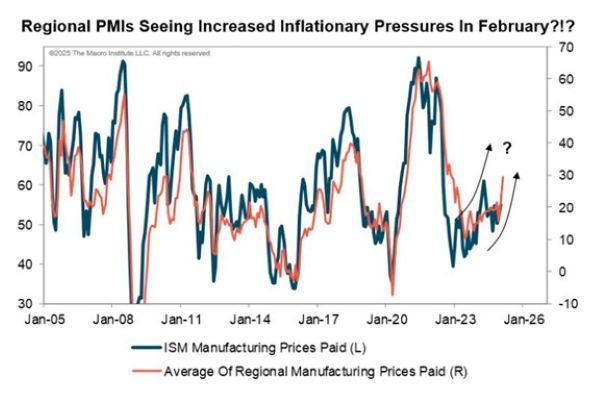

The regional manufacturing price paid indices are gradually rising. This means that inflation seems to want to stabilize around 2.5% in the United States. The housing component continues its downward progression, while the other components are gradually rising.

Price paid index of regional manufacturing indices and ISM prices paid (United States):

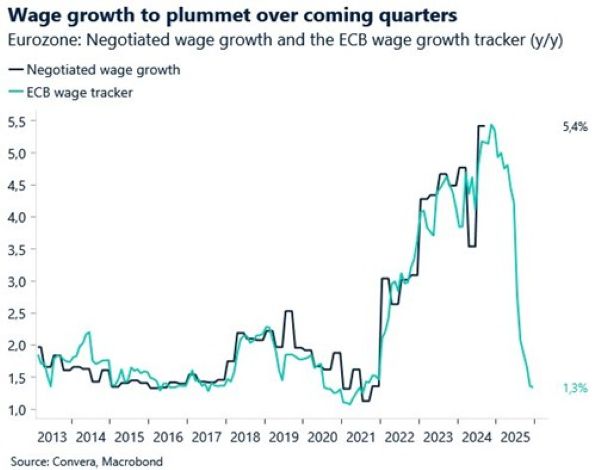

The post-pandemic effects are fading and inflationary pressures are returning to normal. The following chart from Europe is quite telling. The ECB is tracking wage growth in collective agreements. However, we see that agreed wages are falling sharply. These declines will be reflected in next year’s statistics.

European Central Bank wage growth and negotiated wages (Europe):

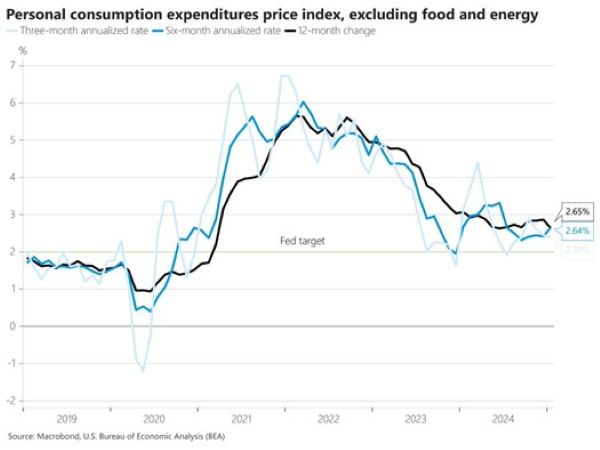

Looking at the Fed’s favorite inflation indicator, the Personal Consumer Goods Price Index, we see stable price growth over the past 6 months.

Personal Consumer Goods Price Index (U.S.):

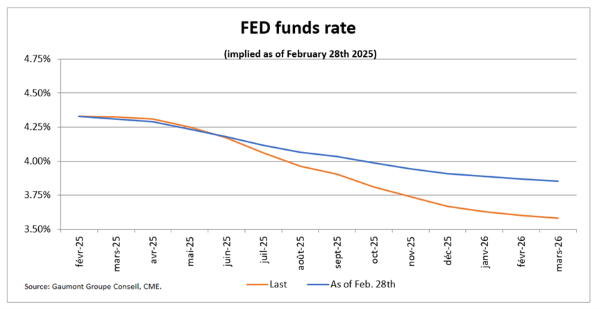

With inflation stable, close to target, the Fed will be able to continue lowering its policy rate this year. A 0.70% cut in 2025 is currently forecast by market participants.

Short-term implied interest rates (US):

Stock Markets:

Looking back, we see that the market dynamics have recently changed. This rotation is healthy and allows the market to continue to move higher.

What is happening?

Professional managers have started to move away from the big growth stocks (Mag7), while retail investors continue to invest in them. The performance gap between the Magnificent 7 and the S&P 493 is close to 10% in 2025.

Performance of the Magnificent Seven and the S&P 493 (United States):

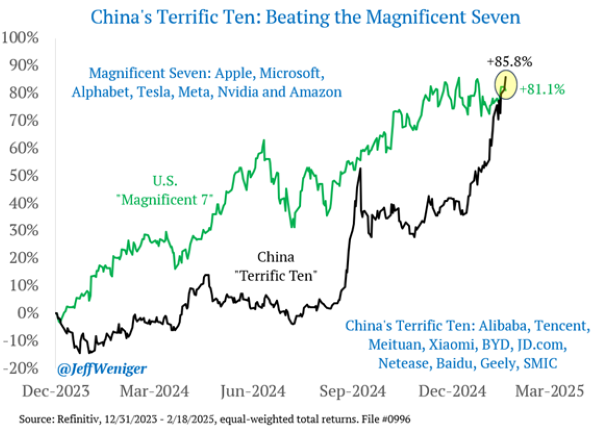

The launch of Deep Seek was the catalyst that propelled Chinese tech stocks into the stratosphere. These stocks were overlooked and heavily undervalued compared to their US peers.

Performance of the Magnificent Seven and Terrific Ten (China):

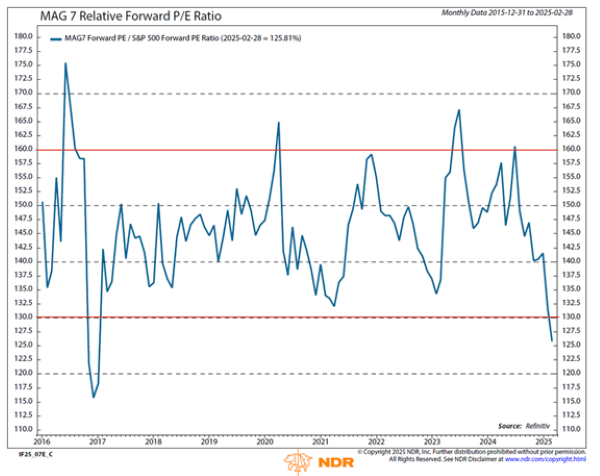

The Mag7’s weak relative performance, compared to the S&P 500 in 2025, has brought the valuation of these stocks (on a relative basis) to the lows of the last 10 years. What about Bitcoin, it is down 25% from its all-time high.

Relative valuation of the Magnificent Seven and US large-cap stocks:

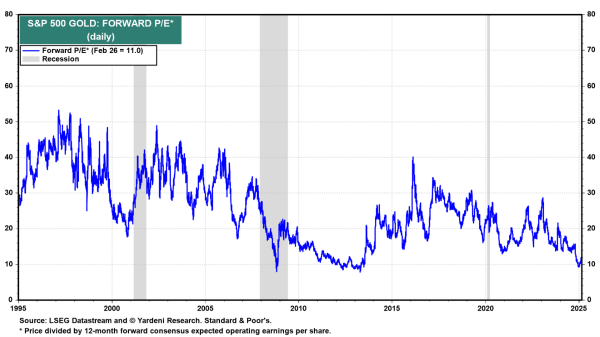

There is also renewed interest in Asian and European stocks. Stocks that have been shunned by everyone, such as gold producers, are also generating sudden interest. These companies are nevertheless very cheap and offer profit margins at their highest in 20 years.

Logic and fundamentals always end up returning to the markets, we just have to be patient.

Evaluation of gold production stocks:

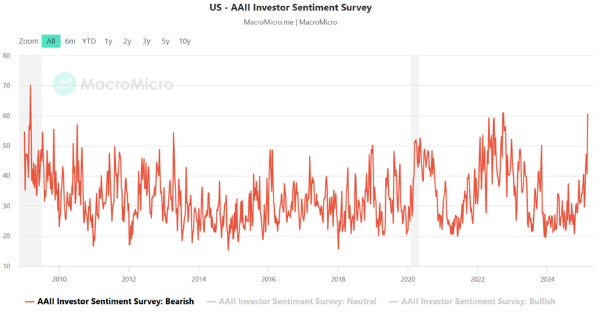

This change in leadership in the stock market is taking place in an environment of marked risk aversion. Retail investors are in panic mode. The level of pessimism is reaching levels rarely seen in 40 years!

Retail investor sentiment towards the US stock market:

CONCLUSION :

The panic we are currently seeing in the stock markets is an excellent opportunity to acquire quality stocks at an attractive fundamental valuation. Risk premiums on bonds also remain attractive.

Frédéric Mercier CFA, SIPC

Director – Financial markets