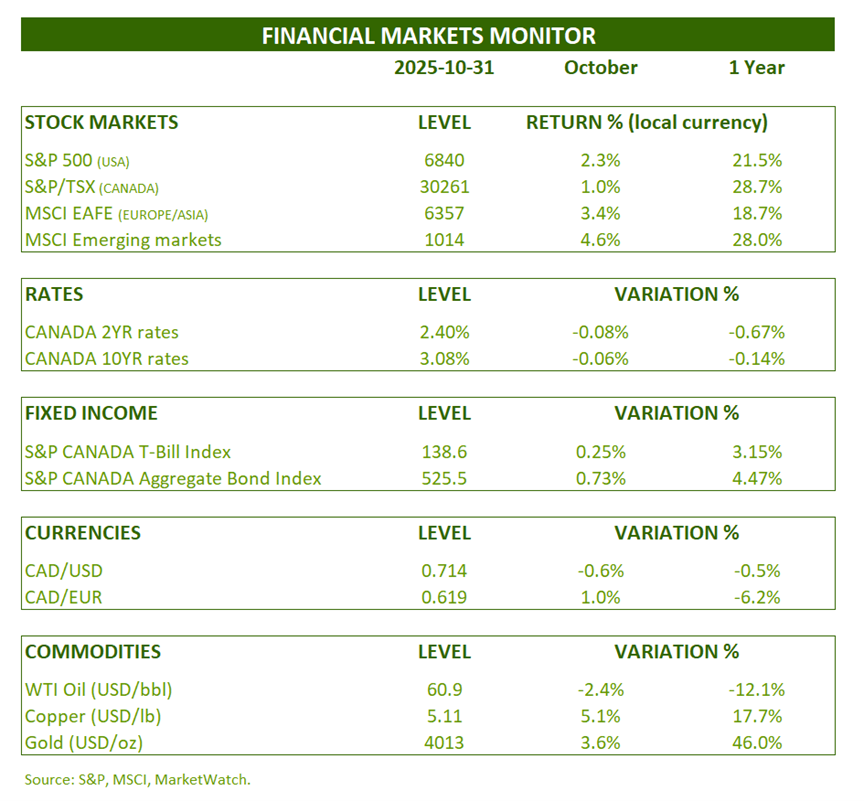

FINANCIAL MARKETS REVIEW

The months are starting to look much the same. For the sixth consecutive month, the S&P 500 has posted positive returns. October saw a gain of 2.3%. The Canadian stock market posted a 1% return in October and a 28.7% return over the past 12 months. Other markets, namely Europe-Asia and emerging markets, also performed strongly, rising 3.4% and 4.6% respectively in October. The underlying themes remain the same. High-beta stocks (riskier stocks) are in high demand, while defensive and low-volatility stocks are being shunned.

Like the Fed (4%), the Bank of Canada (2.25%) lowered its key interest rate in October. It indicated that it no longer expects to cut rates in the short term.

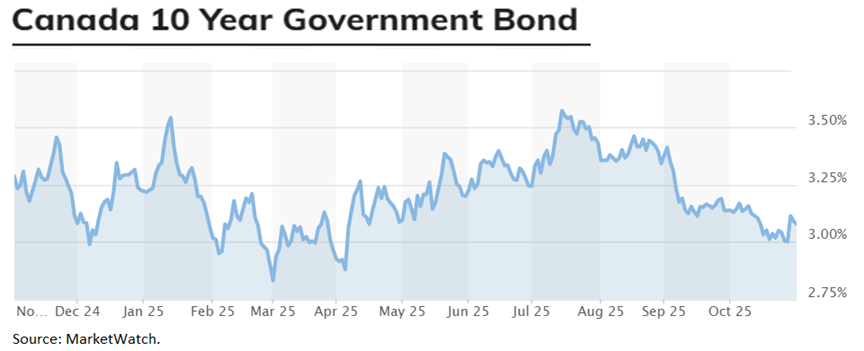

Canadian and U.S. interest rates continued to fall in October. The Canadian 10-year Treasury yield declined by 0.06%. Consequently, the Canadian bond index performed well in October, rising by 0.73%.

OUTLOOK:

Economy:

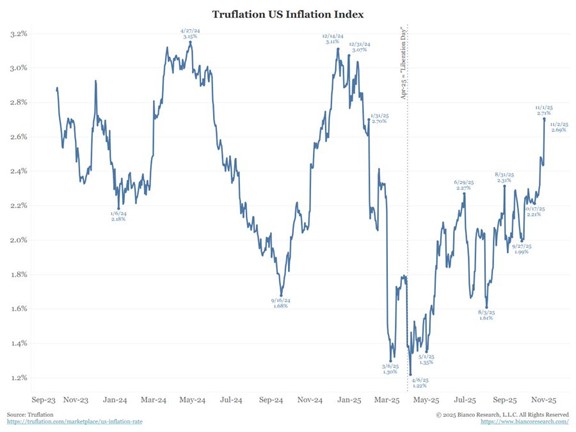

It’s difficult to keep track of the economic situation when the (US) government no longer publishes economic statistics. We have to turn to alternative indicators.

The Truflation website continuously publishes US inflation data. It has continued to rise rapidly since Liberation Day. The most recent estimates conclude that tariffs have had an impact of approximately +0.7% on inflation. This is hardly good news for workers who had enjoyed a respite at the beginning of the year.

Inflation according to the Truflation website (United States):

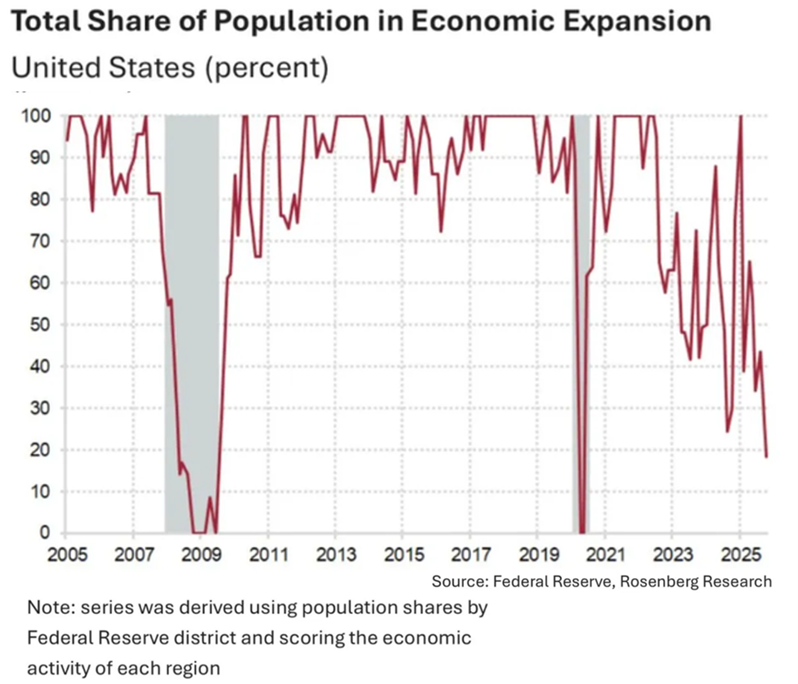

Before each meeting, the Fed receives the Beige Book, a summary of commentary on the current economic situation in its 12 districts. The most recent edition reveals an economy where only 20% of the population resides in a growing district. The population is struggling, which likely explains the high default rate. President Trump’s tariffs are only exacerbating the situation.

Percentage of the population living in a growing district (United States):

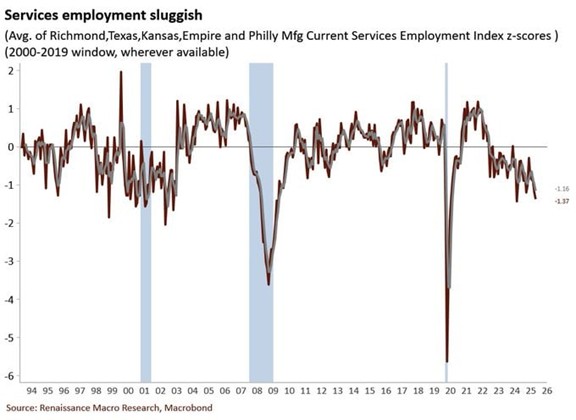

In terms of employment, we consult the manufacturing and services PMI indices to gauge the pulse of the job market. And, like everything else, the job market is depressed. We are near the post-pandemic low.

Regional Services PMI Index (United States):

In Canada, the situation is hardly any brighter. Businesses anticipate stagnant sales over the next 12 months. Furthermore, investment intentions remain very weak.

Data from the Bank of Canada Business Outlook Survey:

Finally, house prices south of the border continue to be under pressure. The oversupply is at a very high level. The good news is that stagnant or falling house prices put downward pressure on the housing component of the Consumer Price Index.

House Supply and Demand (United States):

Fixed Income:

Tariffs will continue to put upward pressure on inflation. This impact is expected to be non-recurring, however, unless tariff percentages continue to rise.

In Canada, a very tight labour market impacted wage-driven inflation in 2022. We are now seeing this effect in reverse. Pressures on production capacity are virtually nonexistent. Historically, in a similar situation, we have seen a reduction in price growth in the following quarters.

Data from the Bank of Canada Business Outlook Survey:

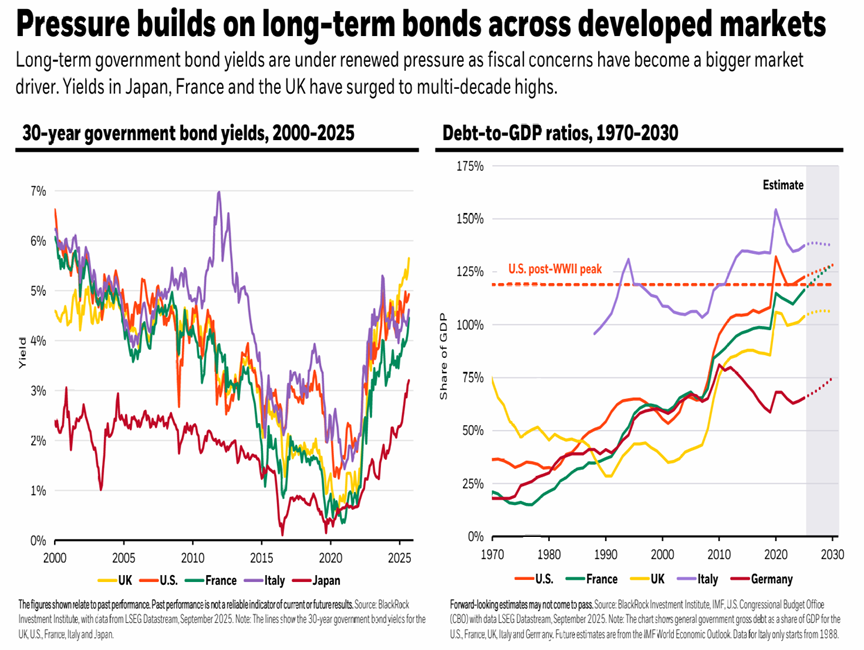

Although these are long-term factors, investors are gradually taking the soaring debt levels seriously. They are now demanding substantial compensation for buying bonds. They are now being paid for the risk they take, which is good news. For governments and taxpayers, however, this means significantly higher financing costs.

Debt of various countries and long-term interest rates.

These offsets are even more evident in the following chart. This chart shows the real interest rate on US Treasury bonds. As of October 31, the real rate was 1.8%. This means that an investor will receive 1.8% plus inflation over the period. This is the true cost of government debt. Central bank purchase programs are used to lower the real rate. We should expect them to use this tool again.

Real interest rate on 10-year bonds (United States):

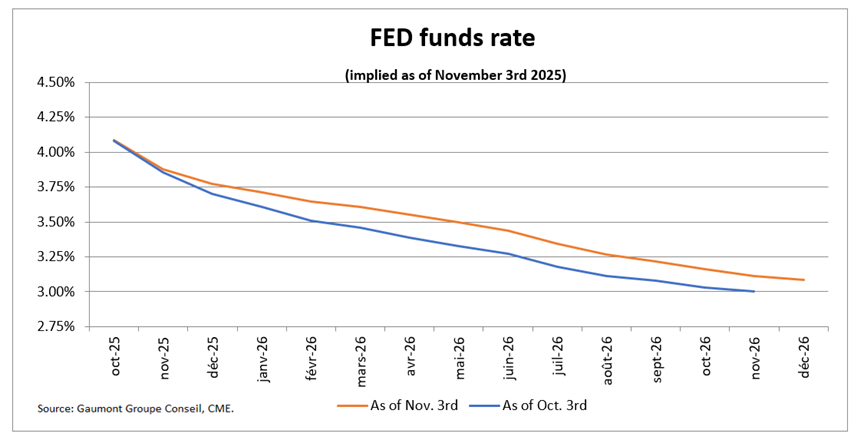

Expectations for Fed rate cuts remained largely unchanged in October. Indeed, cuts of 0.16% are projected by December 2025 and 0.77% within the next 12 months.

Short-term implied interest rates (United States):

Stock Markets:

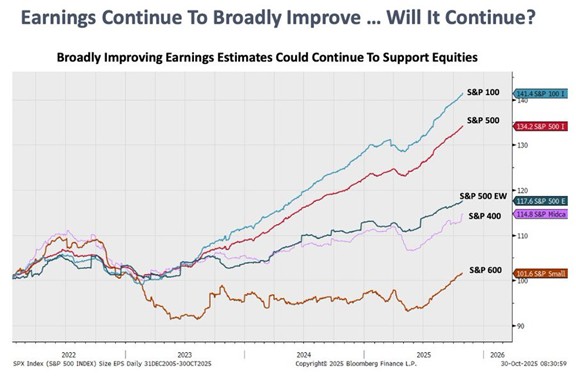

The bull market continues its upward trajectory. The good news is that analysts are continuing to raise their 2026 earnings forecasts. While some of their assumptions, such as margin expansion, may be questioned, the overall trend remains positive.

Earnings Revisions for Stock Market Indices in the United States:

What’s unusual right now is the types of factors that are outperforming. The riskier the stock, the higher its performance (over the last 12 months). The same is true for high-momentum stocks. Conversely, quality stocks are performing very poorly. This indicates that the market is highly speculative and that companies’ fundamentals are currently undervalued. Quality stocks generally outperform over the long term.

This is a great opportunity to reduce portfolio risk by acquiring quality stocks at bargain prices.

Performance of various market factors over the last 12 months (United States):

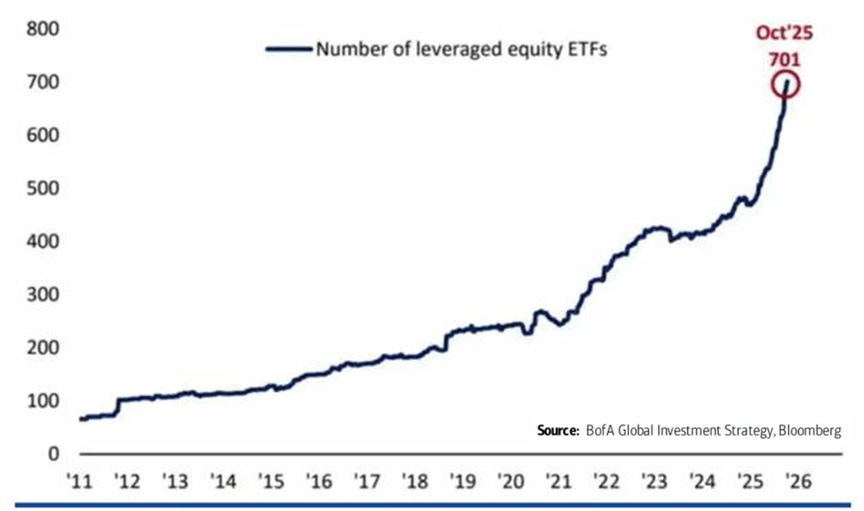

The speculative fervor of the market is easily visualized by observing the following graph. The number of leveraged exchange-traded funds (ETFs), which offer, for example, 3x the return of a stock or index, has doubled in the last three years.

Evolution of leveraged exchange-traded funds (United States):

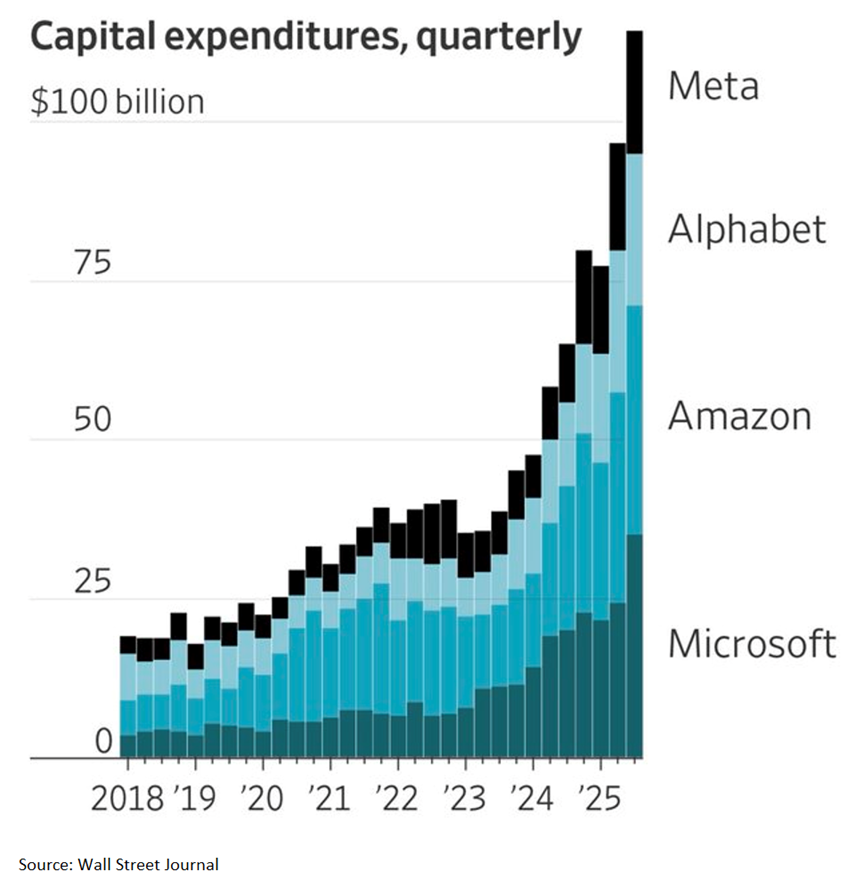

A recent trend that is beginning to capture investors’ attention is the massive investment deployment by major technology players in hyperscale data centers. Some are starting to worry about the colossal sums being invested in AI and data centers. Will these sums generate profits commensurate with the investments? Older generations will remember the fiber optic frenzy of the early 2000s. That frenzy ended badly.

Hyperscale Data Center Investments (United States):

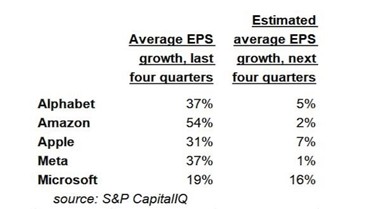

It is noted that the projected profit growth of major technology players will slow significantly over the next four quarters.

Projected earnings for the technology sector (United States):

CONCLUSION :

2025 is an exceptional year for balanced portfolios. We should take advantage of it while it lasts. It is strongly recommended to reduce the weighting of speculative securities and reallocate funds towards quality stocks. These are trading at a significant discount compared to speculative stocks. It’s a topsy-turvy world.

Frédéric Mercier CFA, SIPC

Director – Financial markets