FINANCIAL MARKETS REVIEW

February’s performance can be summed up in one word: dispersion. In the United States, the -0.8% return doesn’t reflect the fact that many sectors generated very strong returns, such as consumer staples (+7.9%) and industrials (+7.1%). Conversely, the software subsector posted a decline of -8.8%. In terms of styles, quality stocks returned 4.7%, while growth stocks fell by -3.4%. Canada achieved a stellar performance of 7.7% in February, driven by basic materials (+21.7%).

Emerging markets and Europe-Asia generated 5% and 5.5% respectively.

Following the release of disappointing job vacancy figures in the United States, coupled with rising employment insurance claims, interest rates declined in February. Indeed, 2-year and 10-year Treasury yields ended the month down 0.17% and 0.30%, respectively.

Consequently, the Canadian bond index performed strongly (1.56%). Gold also had another excellent month, returning 10.6%.

OUTLOOK:

Economy:

The US-Israeli-Iranian conflict began on February 28. At the time of writing, oil prices are up 15%, and stock and bond markets are sharply down. None of this bodes well for the global economy.

If the conflict continues, the soaring price of oil could lead to a supply shock. In the short term, prices rise and growth slows. Moreover, losses in the financial markets could undermine confidence.

Central banks are relatively powerless against supply shocks. Monetary policy primarily operates through demand.

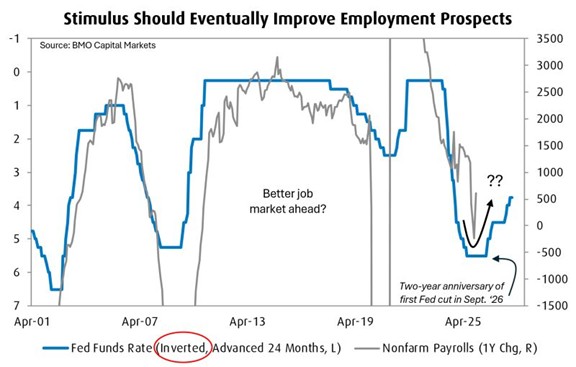

Before the conflict began, the labor market was following the established pattern. Past interest rate cuts continued to have a positive impact on employment and growth.

Policy rate evolution and employment growth (T+24M) (United States):

Past declines in 10-year interest rates suggest continued growth.

Changes in 10-year interest rates and the ISM Manufacturing Index (T+14M) (United States):

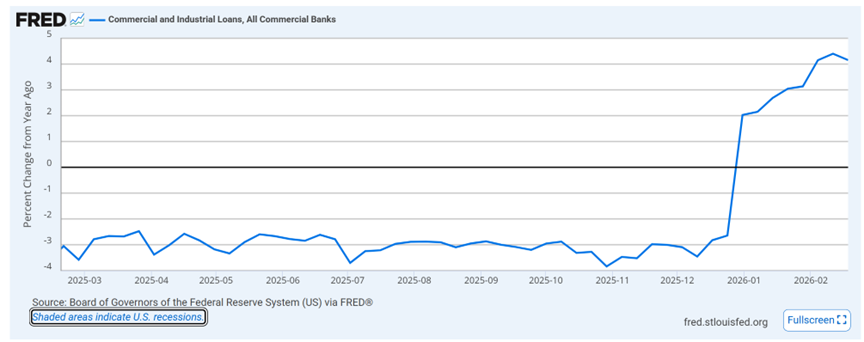

Credit is the lifeblood of the capitalist system. And after two years of stagnation, commercial and industrial lending growth has returned to positive territory. This is a good sign.

Growth of commercial and industrial lending (United States):

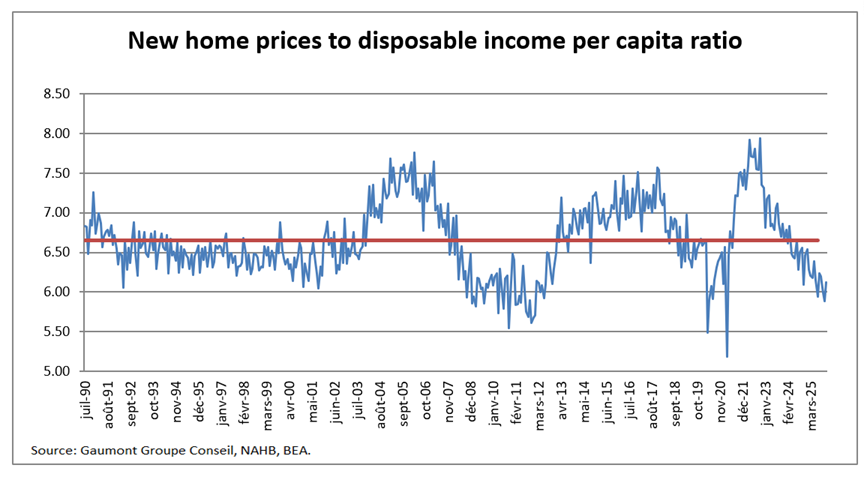

In the US housing market, the decline in mortgage costs could thaw the resale market.

Furthermore, after years of declines or stagnation, prices have returned to near their long-term equilibrium level. Indeed, in the long run, prices follow disposable income. New home prices are even extremely low. This could lead to a more robust construction boom.

Real new home prices adjusted for per capita disposable income (United States):

Fixed Income:

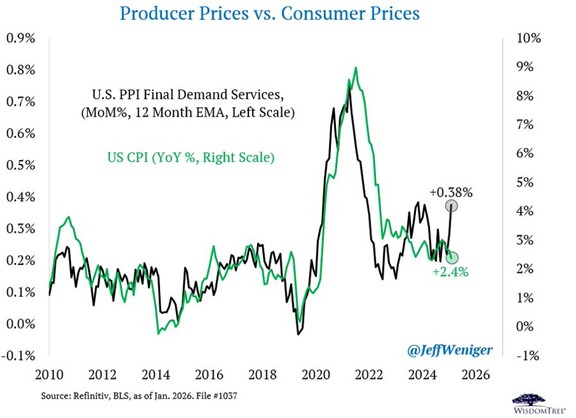

Although inflation remains contained, producer price indices for the past month were up across all sectors, which is something to watch.

Producer Price Index – Services and Inflation (United States):

Expectations of Fed rate cuts were little changed in February. Indeed, cuts of 0.43% are projected by December 2026, compared to 0.47% last month.

In Canada, expectations of rate cuts are at zero by the end of 2026 (91% probability). In fact, the market is pricing in a 9% probability of a 25-basis-point increase this year.

Short-term implied interest rates (United States):

When we talk about interest rates, we’re referring to the nominal rate. However, the true interest rate is the one that takes inflation into account. In the current cycle, the highest real interest rate was observed in August 2023, at 3.18%. The current real rate is 0.85%. Historically, during periods of growth, the low point is around 0%. Therefore, there is still some potential for further decline. In February 2028, the projected real rate is close to zero.

Federal Funds Rate – 1-Year Inflation Expectations from the Cleveland Fed (United States):

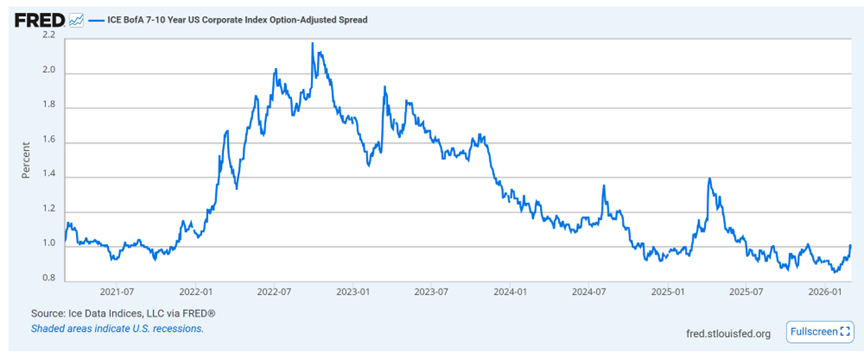

In parallel with stock markets, credit spreads narrowed sharply. Holding corporate bonds offered little return relative to the risk involved. Good news for savers: these returns have rebounded to more attractive levels.

Credit spreads for 7-10 year corporate bonds (United States):

Stock Markets:

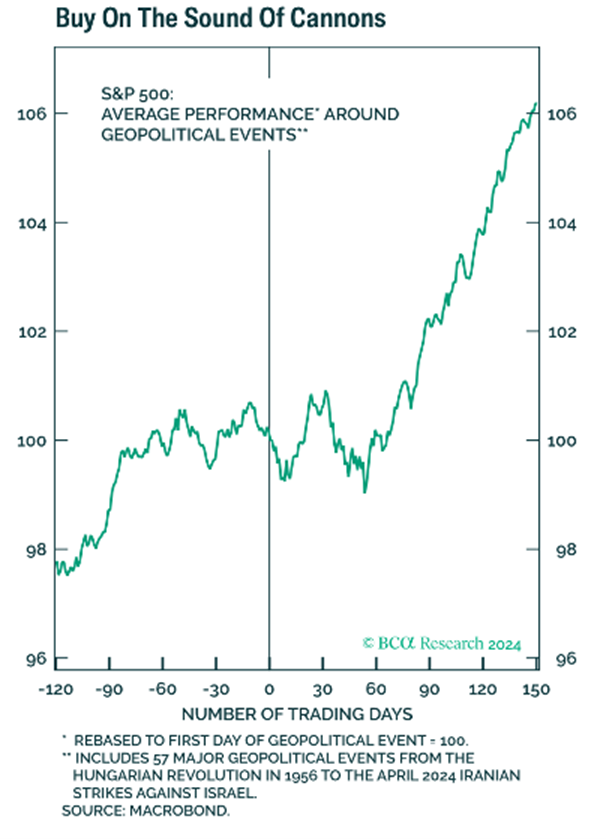

During external shocks such as armed conflicts, investors often instinctively sell first and ask questions later. This creates waves of selling that can generate opportunities. If the conflict continues, investors become accustomed to this pattern. While the outcome of the current conflict cannot be predicted, preparations can be made accordingly. The following chart illustrates the performance of the US stock market during historical geopolitical events. It shows that the market bottoms out within the first 60 days and rebounds after 90 days.

Performance of the US stock market during historical geopolitical events:

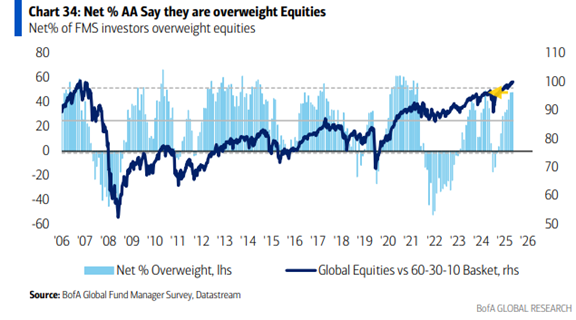

This shock comes at a time when valuations are high. After an exceptional year in 2025, investors are all-in on equities. The following chart shows that their overweight position in equities is very high compared to historical levels.

Evolution of institutional investors’ overweight position in equities – BofA survey (United States):

Over the past five years, US stocks traded at significantly higher levels than elsewhere in the world. However, this premium has now returned to its 2014-2019 level.

Relative valuation of US stock markets compared to the rest of the world:

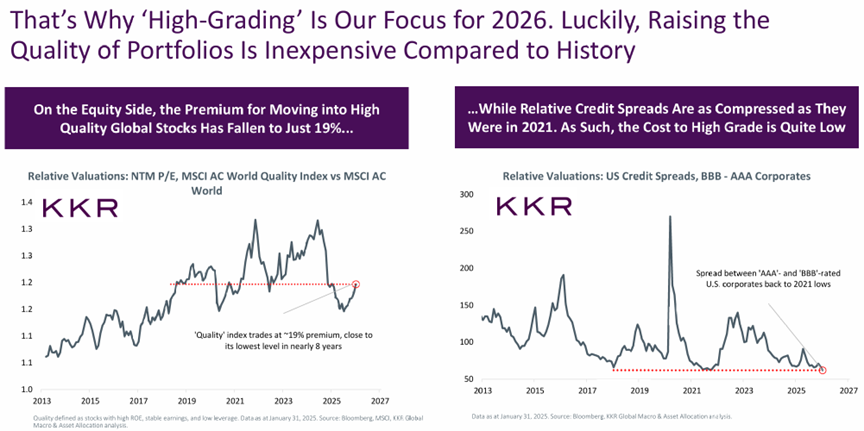

The theme of quality is fundamental to our investment philosophy. However, the price to pay for quality varies over time. For the past few years, the concept of quality has been undervalued. Why hold quality when all securities are rising regardless of their risk? Currently, the concept of quality, in both equities and fixed income, is inexpensive. In the long term, quality outperforms the market in general.

Relative valuation of quality securities – equities and corporate bonds (United States):

CONCLUSION :

Armed conflict makes the economic and financial situation far more unpredictable. What we can control is the resilience and quality of our portfolio. This is not the time to have weak assets in it. Let’s maintain a diversified portfolio of quality securities at reasonable valuations. Let’s remain open to opportunities; it’s often when there’s panic in the air that the best opportunities arise.

Frédéric Mercier CFA, SIPC

Director – Financial markets