COMMENTS

Another negative and volatile month has just ended for stocks and bonds. U.S. and Canadian stock markets fell more than 8% as a diversified portfolio of Canadian bonds fell more than 1.9% during the month. The world’s monetary authorities are demonstrating that they are determined to quell inflation at any cost (including a recession). Thus, the Fed (US Central bank) raised its key rate at an increasingly high rate, ie an increase of 0.25% in March, 0.50% in May and 0.75% in June.

Yields in Europe/Asia and Emerging Markets were slightly better with respective performances of -6.3% and -4.6% during the month.

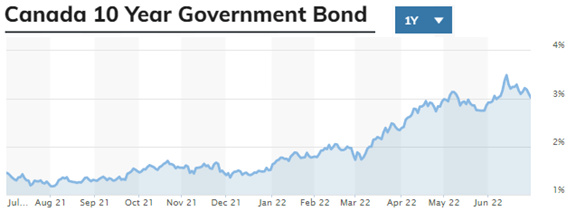

10-year interest rates exploded upwards in the first half of the month (+0.74%) before falling by 0.38% thereafter. The increase was therefore 0.36%, which is still considerable.

The S&P Canadian Diversified Bond Index has generated a return of -10.4% for one year.

PERSPECTIVES :

Fixed income:

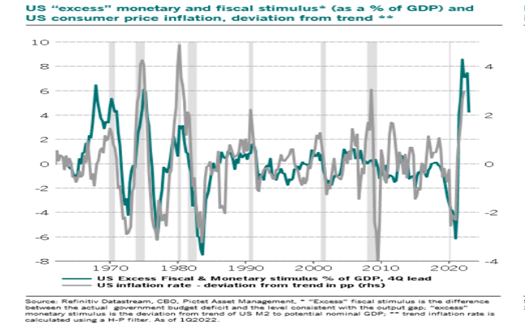

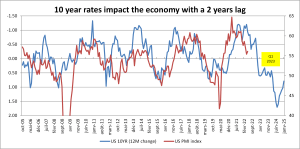

In retrospect, monetary and government authorities took no chances during the pandemic and overstimulated the economy and markets (see next chart). Now, in their own way, they are trying to put the toothpaste back in the toothpaste tube! It is a very difficult task that cannot be done without breaking eggs. Interest rates are back to where they were in 2019 and stocks are slowly getting there.

This overstimulation had a direct impact on inflation for consumer goods and services and financial assets. This is what central banks are currently fighting with ardor.

A recession has always been a good remedy against inflation caused by excess demand (blue and yellow in the following chart). For supply-side effects, monetary policy has little effect.

This is where we seem to be headed, a recession.

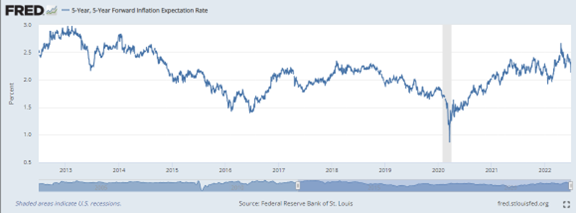

The good news is that medium to long-term inflation expectations are slowly converging towards their pre-pandemic level. This means that investors believe that inflation will not be a problem in the long term.

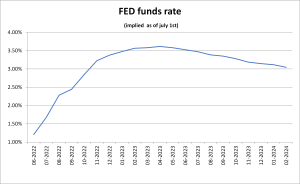

Canadian financial markets are currently reflecting short-term interest rates (which should prevail) of 3.5% as of December 31, 2022. South of the border, they should be 3.3% at the end of December.

So, although there are still several rate hikes to come between now and the end of the year, the market does not anticipate any more hikes in 2023, but rather falls in late 2023 early 2024. The recession is practically already anticipated by market participants.

Our long-term leading indicators are already pointing in that direction. The economy is expected to continue to weaken through the first quarter of 2023.

Signs of a slowdown are becoming more and more visible day by day. At this point, it is difficult to see the banks becoming more aggressive than they are now. Therefore, the damage to bond portfolios is likely behind us.

Stock markets:

We can simplify the change in the price of shares into 2 components:

• Changes in the price/earnings ratio (P/E ratio)

• Profit growth

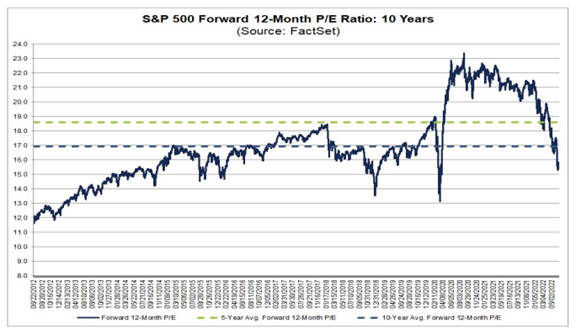

The normalization of interest rates has in turn led to a normalization of the price/earnings ratio. As the following chart shows, the price/earnings ratio is highly correlated to rates.

This ratio is now slightly below its 10-year average. So, no more bad surprises on this side.

As for earnings growth, it is strongly linked to the economic activity of the country.

However, a slowdown is underway and, possibly even a recession, earnings projections are still on the rise (see the following chart). There seems to be something wrong!

However, the confidence of business leaders is melting like snow in the sun. This generally bodes ill for earnings, as evidenced by the following chart.

Historically, inventory management has been the cause of many recessions. The following table presents the growth (over the last 4 quarters) of sales and inventories of large chain stores in the United States. We see that inventories have increased much faster than sales. So stores are selling off inventory, reducing orders, and manufacturers are reducing production. This is only one line of business, but it demonstrates a downturn/recession dynamic.

Earnings will likely be revised down in the coming quarters. These generally drop by 15-20% during recessions.

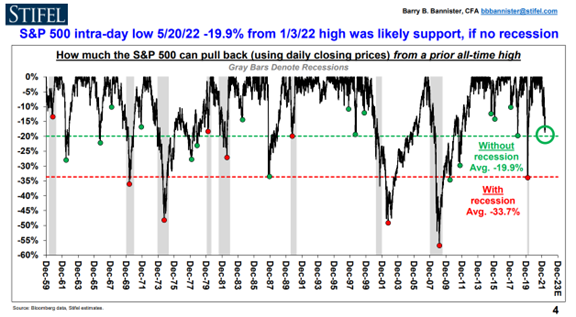

So we may not be out of the woods for the stock markets. Historically, recession-free corrections average -19.9%. Which is close to the current drop of -21%. If the recession materializes, an additional drop of 15% is possible.

CONCLUSION :

Central banks continue to tighten financial conditions, but that no longer surprises the bond market. The worst is probably behind us for bonds. At the stock market level, profits will likely be revised downwards, in parallel with the economic slowdown. Caution remains in order with regard to this asset class.

Frédéric Mercier CFA, SIPC

Director – Financial markets