FINANCIAL MARKETS REVIEW

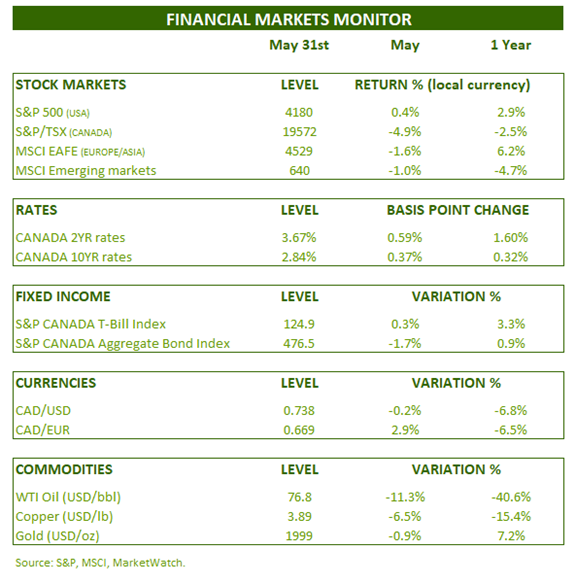

Despite better-than-expected profits, the US stock market stalled (+0.4%) in May. In Canada, the sharp fall in the price of oil (-11.3%) and raw materials weighed heavily on the Canadian stock market. The Toronto Stock Exchange index has lost nearly 5% in the past month. Stock market levels are maintained by only a handful of securities, mainly in technology, including, for example, those related to artificial intelligence.

As for interest rates, they rose sharply in May. Indeed, inflation is falling less rapidly than expected and some employment data remain resilient. 2-year interest rates climbed 0.59%, indicating a possibility that the Bank of Canada may continue to raise its key rate (increase of 0.25% on June 7, 2023). As for 10-year rates, they rose by 0.37% during the month. These rate increases had the effect of bringing the Canadian diversified bond index into strongly negative territory (-1.7%).

OUTLOOK:

Economy :

Leading indicators for the US economy continue to weaken. The following graph shows us the evolution of the leading indicator of the Conference Board.

Leading indicator (LEI) and recession (USA):

The Chicago PMI gives us the same signal. We are almost certainly in a recession right now. Many statistics show a stagnation for 6 months such as industrial production and personal income.

Chicago PMI index – recession (USA):

The job market is usually the last bastion to fall into a recession. Job creation remains strong in the United States. However, looking under the hood and other indicators, we see that it is not as strong as it seems.

Job market (USA):

An unusual element that prolongs the current cycle a little is the excess savings generated during the pandemic. In the following graph, we see that the pandemic has enabled households to significantly increase their savings. Now, the impacts of rate hikes and inflation are rapidly eating away at those savings. It is estimated that excess savings will be exhausted by the end of the year. Once elapsed, the awakening could be brutal for households.

Excess Pandemic Savings (USA):

Despite this savings cushion, car delinquencies are climbing rapidly for all age groups.

Defaults on credit cards (USA):

Increasing defaults lead to tighter credit conditions for banks. This tightening is not limited to the United States, it is global and is dangerously close to the level of 2002 and 2008.

Global Credit Terms:

The following graph shows us the imbalance in American real estate. The gap between the cost of buying and renting has never been higher. A decline in house prices is virtually inevitable. The sector will remain under pressure for some time.

Real estate market (USA):

Fixed income:

As we know, inflation is a lagging indicator. For this reason, we know that the pace of inflation will continue to decline for at least another year. This decline does not seem fast enough in the eyes of the Fed.

Expected NFIB Price Increase and Inflation (USA):

Although we are skeptical, the market anticipates the possibility of a final rise within 3 months. We are exactly at the level of rates that the Fed has been telegraphing since December.

Short-term interest rate (USA):

Assuming the last rate hike occurred in May, one would expect the Fed to start cutting rates rapidly in early 2024. As the following chart shows, rate cuts begin usually 6-7 months after the last rise.

Rate cut after a break (USA):

With the recent rise in 10-year rates in Canada, rates on quality Canadian corporate bonds have also risen. They reached 5.24% at the end of May. In this period of uncertainty, it is an interesting way to generate returns without too much risk (the average maturity is around 7 years).

Interest rates on quality Canadian corporate bonds:

Stock markets:

The stock market remains very resilient despite the recession, the debt ceiling debate, bank failures, etc. The following graph shows this important dichotomy. On the one hand, investors are almost all anticipating a weaker economy, but at the same time, the US stock market is doing well.

Growth expectation and return of the S&P 500:

What is going on ? Stock market gains are concentrated in a handful of 7 tech stocks. The other 493 stocks had a return of zero in 2023. This is an indication that market progress is based on little.

Return of the S&P 500 year to date:

Like the tech bubble of 2000, money is flowing into tech stock funds. The new carrier theme is now artificial intelligence and the new flagship is the Nvidia company. There is no doubt that artificial intelligence could generate many benefits for society and profits for companies. However, one should never lose sight of the valuation of securities. Nvidia is currently trading at 35X SALES! In 1999 Cisco was trading at 38X sales in 1999 and now at 3.7X.

Fund inflows – technology stock funds:

Another surprising element is that (high-growth) technology stocks are very sensitive to the discount rates (10-year interest rate) of their cash flows. However, rates have risen significantly without really impacting the price of Nasdaq securities. The divergence can be seen in the following chart.

Nasdaq and 10-year interest rates:

Finally, when rates rise and the long-term stock market outlook declines (valuation too high), the risk premium for holding this asset decreases. This means that the investor is paid little for taking on additional risk. The following graph shows us that the risk premium is historically very low.

Risk premium on US equities:

CONCLUSION :

The current uncertainty and high valuation make the stock market unattractive. High interest rates allow you to generate an attractive return without taking too much risk. The watchword remains patience. Investors are well paid to wait for opportunities to arise and for risk premiums to be more attractive.

Frédéric Mercier CFA, SIPC

Director – Financial markets