FINANCIAL MARKETS REVIEW

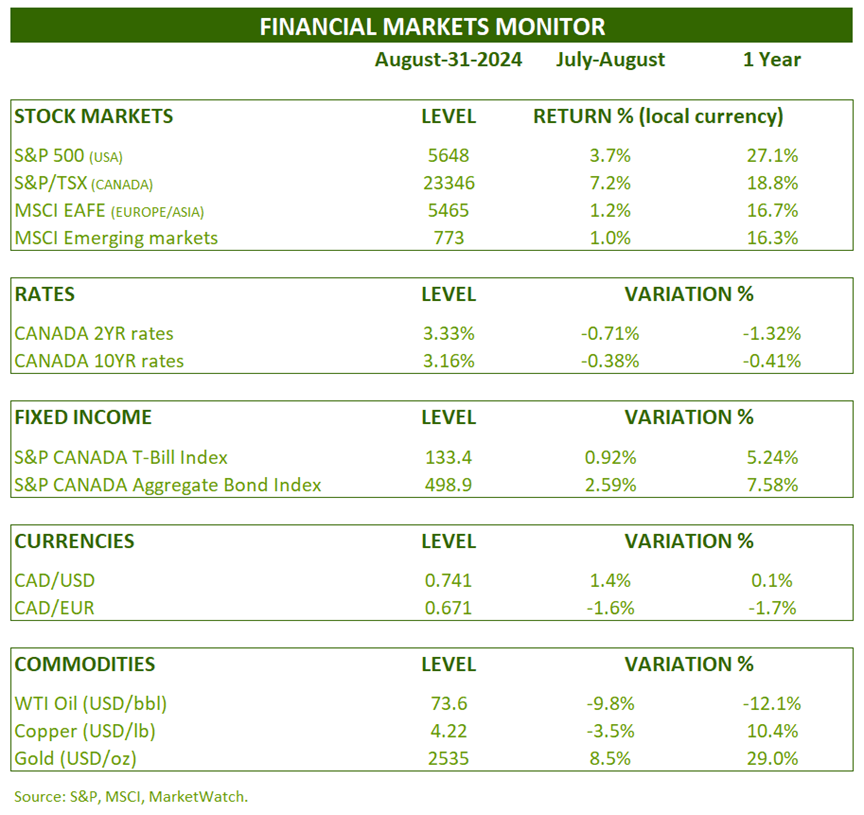

Global stock markets continued to perform well this summer. Both Canadian and U.S. indices hit new highs. The S&P 500 index rose 3.7% in July-August, while in Canada, performance was explosive at 7.2%. Little by little, the leadership is changing in the stock market. While the technology sector is struggling, small caps and other stocks in general are doing well.

Inflation data continues to trend in the right direction. In Canada, core inflation is at 2.7%, while excluding housing is at 1.8%. That’s why the Bank of Canada can now afford to cut its rate. It has been cut by 0.75% since June. In the United States, the first rate cut is expected to occur on September 18.

This drop in inflation in Canada has boosted expectations of rate cuts. The 2-year maturity has seen its rate drop by 0.71% over the past 2 months. For its part, the 10-year rate has dropped by 0.38%. These sharp rate cuts have propelled the yield on the Canadian bond index to 2.59% for the 2 months.

OUTLOOK:

Economy:

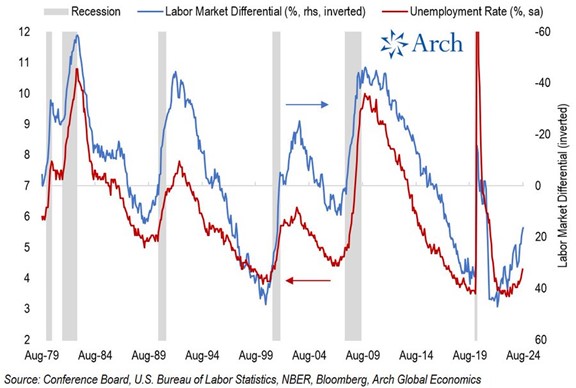

The unemployment rate has continued to rise in the United States and leading employment indicators point to further deterioration in unemployment. Indeed, the Conference Board’s survey of the level of difficulty in finding a job continues to deteriorate at a pace only seen during a recession.

Level of difficulty in finding a job and unemployment rate (United States):

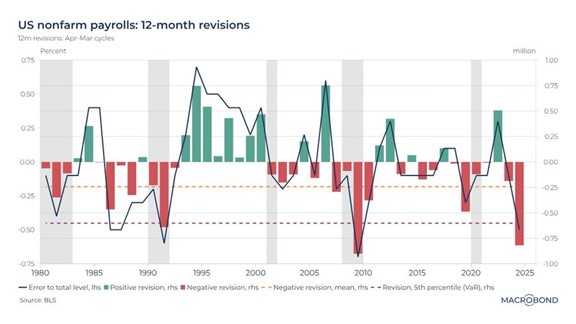

In addition, in their annual revision, the BLS (Bureau of Labor Statistics) lost 818,000 jobs in the last 12 months, or 31%. This confirms what we have been saying for a while, the American labor market is much weaker than it appears. The data will probably be revised again in the coming years. This is not bad will on their part, but it is very difficult to see sudden changes in real time. What we do see, however, is that large revisions in employment occur during recessions.

Annual revision of employment data (United States):

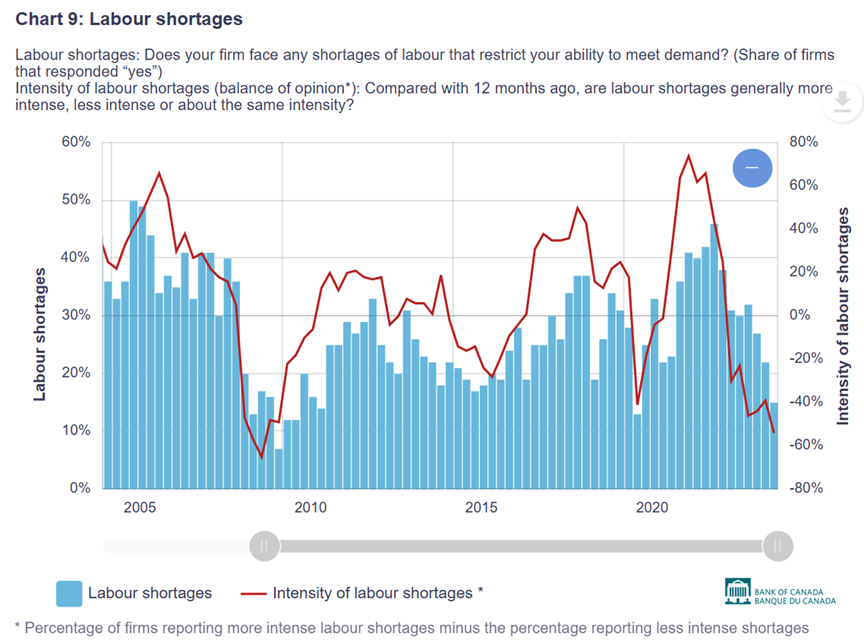

In Canada, data from the Bank of Canada’s Business Outlook Survey informs us about the labour shortage. However, there has been a 180-degree turnaround since the end of 2021. Globally, we are currently experiencing the opposite of a shortage. The level of difficulty businesses are having in finding labour is flirting with historic lows. This goes hand in hand with very weak wage growth.

Labour shortage (Bank of Canada Business Outlook Survey)

Consumer confidence is important for household spending. What we see is that consumers have moderate confidence now, but very low confidence for their situation in 6 months. This confidence gap is strongly negative and generally coincides with recessions.

Consumer confidence: current situation and expectations in 6 months (United States):

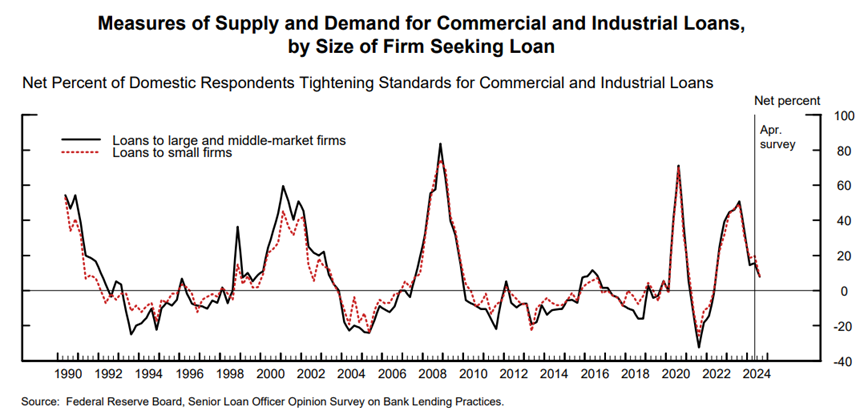

Finally, credit conditions for businesses and consumers are gradually returning to their historical averages. This is very good economic news, but its impact will not be felt for 9 to 12 months.

Business Credit Conditions: (United States)

Fixed Income:

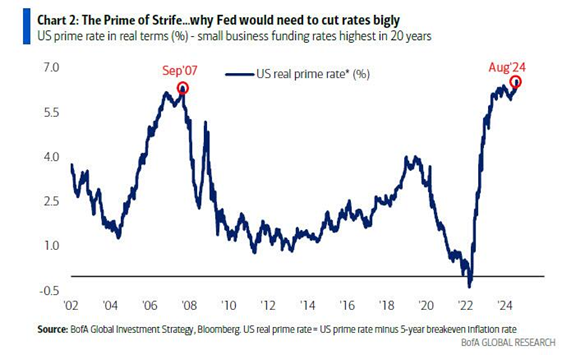

Falling inflation is good for the economy in general. However, this good news hides another. By keeping its key rate fixed, while inflation is falling, the FED is helping to increase real rates (net of inflation). To this end, the current real prime rate is at its highest level in over 20 years. This will continue to put pressure on the economy, but also on the FED.

Real prime rate (United States):

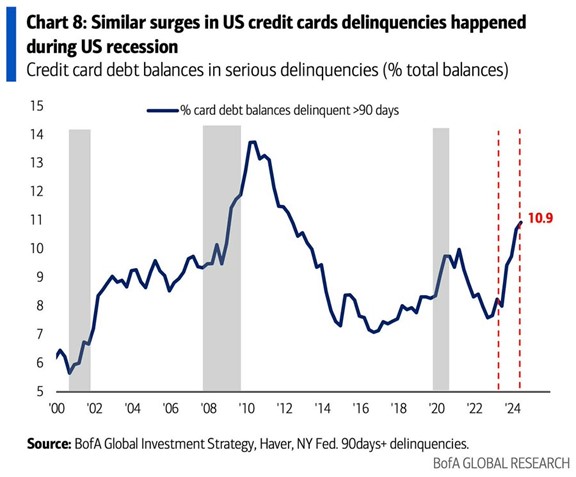

With real rates strongly positive, it is not surprising to see credit card delinquencies continue to rise. This is not a good sign for consumer health and it puts pressure on banks’ asset quality.

Credit Card Default Rates (US):

Rate cut expectations have increased sharply since the last market review in June, with cuts expected in 2024 increasing by 0.5% and by 1% for the next 12 months.

Short-term implied interest rates (US):

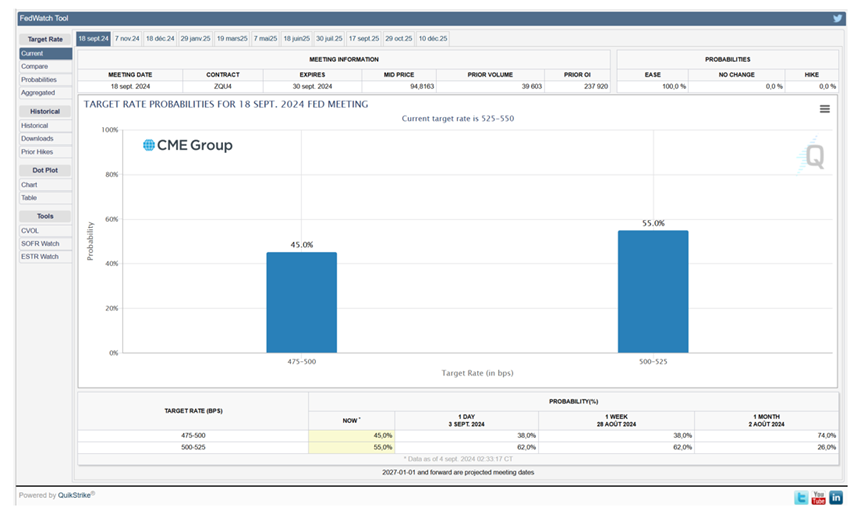

For the Fed meeting on September 18, markets are giving almost as much probability to a 0.50% cut as to a more traditional 0.25% cut. Remember that rate cuts have an impact on the economy, but with a lag of 12 to 18 months.

Probability of a FED rate cut on September 18 (United States):

Stock Markets:

The US stock market continues to rise, but the euphoria has taken a break. Indeed, the Magnificent Seven have been rising less quickly than the rest of the stock market since May.

Despite this, US stocks remain very expensive and are particularly vulnerable to a deceleration in earnings or a more cautious attitude towards risk-taking. The compensation for taking risk (risk premium) in US stocks remains low from a historical perspective. However, high valuations are not indicators of timing.

Price-earnings ratio and risk premium of the S&P 500:

Performance by the Magnificent Seven (USA):

In addition to being expensive on an absolute and relative basis, the biggest problem with US stocks right now is their decoupling from the current economic environment.

In the following chart, we see that cyclical stocks have been outperforming defensive stocks royally over the past year, which happens during strong economic expansion. However, this is not the case. The ISM Manufacturing Index remains at 15-year lows.

Relative performance of cyclical vs. defensive stocks and the ISM Manufacturing Index (US):

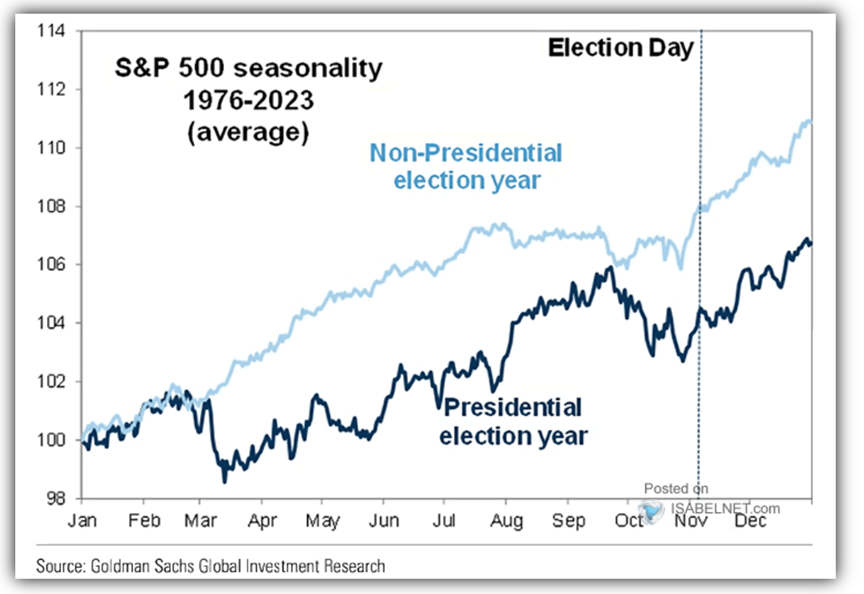

We are starting the month of September, which is historically the only month of the year that is negative on average. In addition, the period from September to early November is a period of stagnation, more so in a presidential year.

Seasonality of the American stock market (S&P 500):

Finally, stock markets almost always start when the Fed pivots and begins its rate cut cycle. This is not a prediction, but a non-negligible possibility. Bear markets often start when valuations are high (US) and there is euphoria in the air (AI).

At first, stock markets celebrate the rate cut (lowering the discount rate), but investors quickly realize that if the Fed cuts rates, it means the economy is in trouble and corporate profits are at risk.

FED pivot (1st cut after a rate hike cycle) and bear market (US):

CONCLUSION :

Risky assets are trading at high valuations given the economic environment and risks. At current rates, bonds remain more attractive than equities. As the impacts of past rate hikes dissipate (excluding the US), opportunities could arise during corrections. We will need to be prepared to deploy capital to equities in a timely manner.

Frédéric Mercier CFA, SIPC

Director – Financial markets