FINANCIAL MARKET REVIEW:

Global stock markets celebrated the ceasefire with Iran in April. After ending March down 5%, the S&P 500 index surged with a 10.5% gain. The Canadian stock market, meanwhile, generated a return of 3.8%.

Emerging markets, being the hardest hit by the closure of the Strait of Hormuz, experienced a strong month with gains of 13.3% (including a 2.8% appreciation of their currencies). Europe and Asia also performed well, posting a 5.1% gain in April.

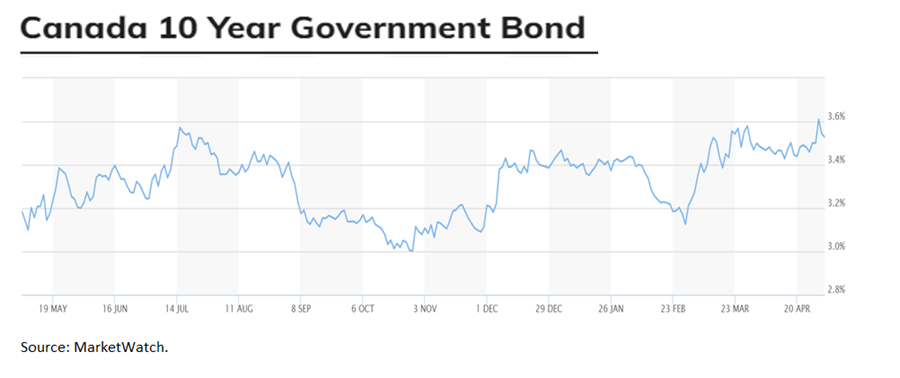

Interest rates were highly volatile throughout the month, but they continued the upward trend from the previous month. Indeed, 2-year and 10-year maturities ended the month higher, with respective increases of 0.13% and 0.07%.

Consequently, the performance of the Canadian bond index finished slightly higher, at 0.21%.

Oil prices continued their upward trend in April, after rising 51% in March. They closed up 3.6%. North Sea crude (Brent) is trading at its highest level since the start of the conflict ($111).

OUTLOOK:

Economy:

At the beginning of each month, we receive various Purchasing Managers’ Index (PMI) readings from around the world. These are valuable leading indicators of global industrial production. The global manufacturing PMI reached 52.6 in April, compared to 51.3 in March. This is the highest level for the index since March 2022. The war with Iran thus appears to have had a mixed impact so far.

S&P Global Manufacturing PMI Index:

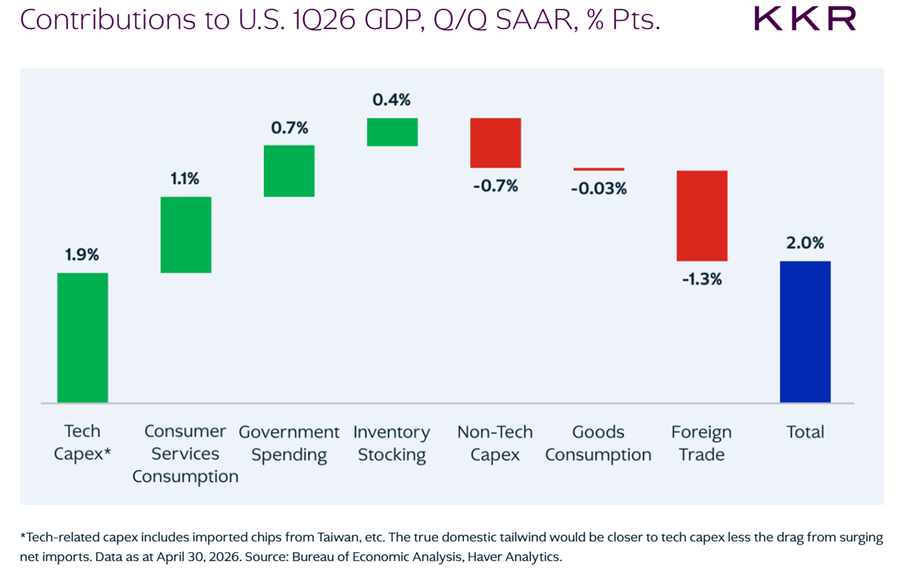

We got our first glimpse of US economic growth last week. Real GDP grew at an annualized rate of 2%, compared to expectations of 2.2%. This growth can be considered adequate. It’s the details that may be surprising. Almost all of the growth can be attributed to investment spending by technology companies. Conversely, consumption of goods contributed nothing to GDP, even though it represents nearly a third of GDP. This is the fifth consecutive quarter in which we have observed this trend.

Contribution to GDP in the first quarter of 2026 (United States):

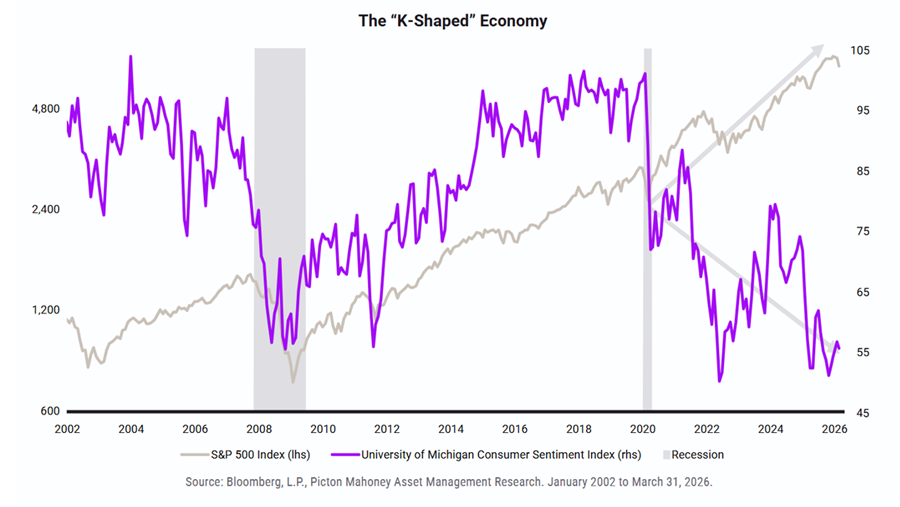

We are hearing the term « K-shaped economy » more and more from economists. This means that within the same economy, one segment of the population is getting richer while another is struggling.

The more educated segment benefits from the ever-rising stock market. Their confidence is high, and they consume heavily. Conversely, unskilled workers are struggling, and their confidence is abysmal. Added to this is the recent rise in gas prices.

This dynamic is illustrated in the following graph: The US Stock Market vs. Consumer Confidence.

The « K »-shaped economy in the United States:

The job market remains stable, but it is still precarious.

Layoffs and employment insurance claims remain low, but hiring is plummeting. This does little to boost consumer confidence.

The American job market:

With the race for artificial intelligence, investment spending will continue to grow at a breakneck pace and is expected to continue making a significant contribution to GDP.

In the short term, the K-shaped economy could hold steady.

Investments in artificial intelligence 2026-2031:

In the medium and long term, net investment in capital and research and development translates into increased worker productivity two to three years later.

Increased productivity is the key factor in raising a population’s standard of living. Increased productivity means doing more with less. Companies can therefore raise wages without impacting inflation.

Investment in R&D and productivity (T+24M) (United States):

Fixed income:

The war with Iran could disrupt supply chains worldwide and directly impact inflation. So far, the impact remains small, as evidenced by the monthly indicator measuring the strain on global supply chains developed by the Federal Reserve Bank of New York.

Monthly indicator measuring the strain on global supply chains (United States):

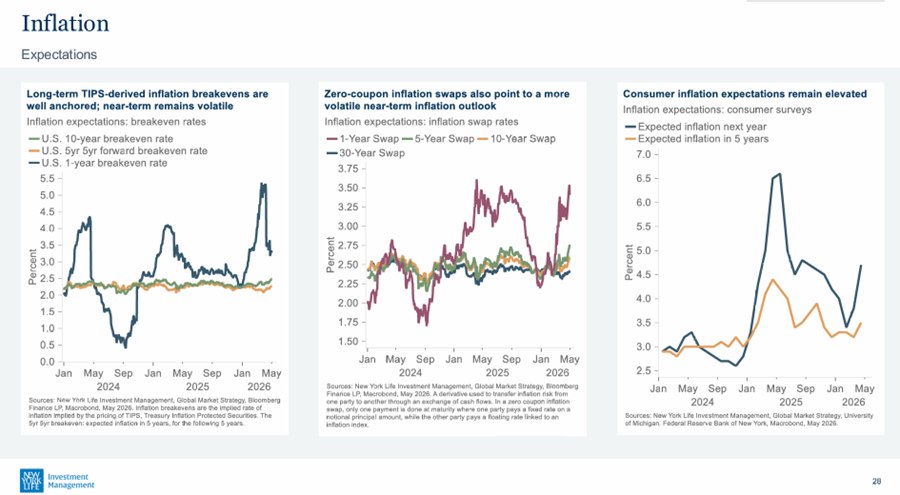

One of the factors central banks monitor is medium-term inflation expectations. They want these expectations to remain within their target range. Their credibility is at stake.

Currently, medium-term expectations are subdued, as the following charts illustrate.

Implicit inflation (United States):

Expectations of Fed rate cuts evaporated in March and remained stable in April. Rate cuts in 2026 are no longer on the table at all. Perhaps a 0.06% increase in the first half of 2027.

In Canada, rate expectations now point to a 0.47% increase by the end of 2026.

Short-term implied interest rates (United States):

Stock Markets:

Euphoria, panic, and euphoria. That’s how one could summarize stock market activity in 2026. April was a reward for disciplined investors who kept their cool and made purchases in March. The ceasefire, along with strong corporate earnings, were the catalysts. We are reaching new highs.

First-quarter S&P earnings have been significantly revised upwards in recent weeks. As of December 31, earnings were projected to grow by 12.5%. By May 4, with two-thirds of companies having reported their results, the projected growth was now 27.1%, a five-year high.

S&P 500 earnings growth for the first quarter of 2026 (United States):

Where does this strong profit growth come from? Revenues are soaring, while profit margins are reaching record highs. A perfect match. The technology sector is seeing growth exceed 50%, but most other sectors are also performing very well.

High margins and profits are a global phenomenon. In Europe, margins are at their highest level in at least 25 years.

Profit margins in the United States and Europe:

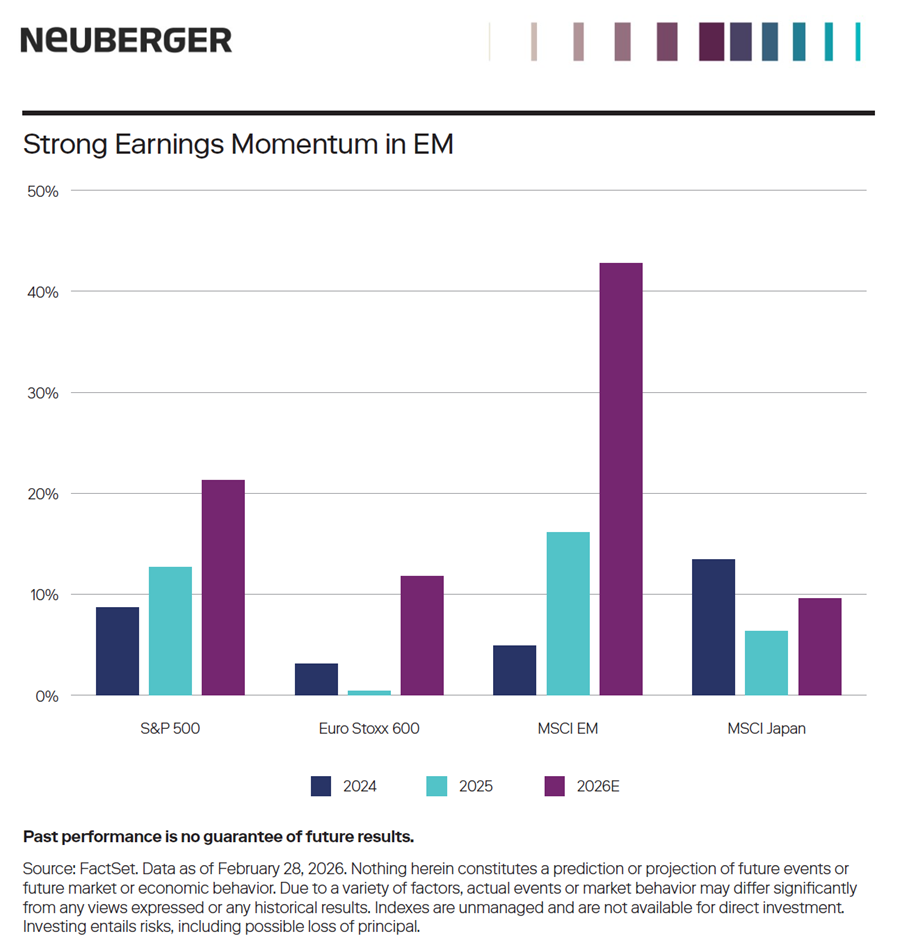

In terms of profit, emerging markets took the top spot in the first quarter with profit growth exceeding 40%.

Annual Corporate Profit Growth – Various Regions:

In the short term, signs of euphoria are slowly emerging. As the following graph shows, inflows into risky assets have exploded in recent weeks.

Fund inflows into risky vs. safe assets (United States):

CONCLUSION:

The conflict in the Middle East brings its share of volatility. We must remain vigilant to seize opportunities. A rebalancing towards bonds could be appropriate. Recent interest rate hikes make bonds even more attractive.

Frédéric Mercier CFA, SIPC

Director – Financial Markets