FINANCIAL MARKETS REVIEW

Although equity returns were generally positive during the month of March, volatility was nonetheless significant. The US stock market ended up 3.7% while the S&P/TSX ended down slightly (-0.2%).

This volatility was caused by the bankruptcy of 2 American banks, Silicon Valley Bank and Signature Bank. We will come back to it.

Fears about the stability of the financial system drove rates down sharply across the curve. Canadian 2-year maturity rates (very sensitive to monetary policy) fell sharply (-0.46%). As for 10-year rates, they fell by 0.44% during the month. The Canadian diversified bond index offered a strong return of 2.05%.

OUTLOOK:

Economy :

The bankruptcy of 2 American banks, whose combined assets totaled more than $325 billion, is certainly not trivial. Was it predictable? Yes and no. It is often said that the Federal Reserve raises its rates until something breaks in the financial system. The following graph demonstrates this. So, given the magnitude and speed of the rate hikes, we expected something to happen, without necessarily knowing what.

The good news is that the American authorities reacted quickly to avoid contagion. However, other mishaps could occur in leveraged or interest rate sensitive sectors. Residential and commercial real estate are sectors at risk.

Rate increases and financial accidents:

The availability of credit was already very limited before the two bankruptcies. These events will only make things worse. Usually, when the FED puts programs in place to make it easier to borrow from banks, the conditions tighten up sharply.

Bank borrowing from the Fed and credit terms:

The tightening of credit conditions is starting to impact loans to banks, but with a delay of 4 quarters.

Credit condition and loan from banks (USA):

Access to credit is the cornerstone of market economies. So, when the price (interest rates) and the quantity of available credit are restricted, the repercussions on growth and the price of assets are direct. The following 2 charts show the negative impact on corporate defaults and the rising unemployment rate.

Credit conditions and corporate default:

Credit conditions and unemployment rate:

At the risk of repeating ourselves, leading indicators should drive portfolio management and NOT coincident or lagging data. One of the most important indicators in our toolkit is the impact of past rate hikes, consistent with the idea that monetary policy percolates through the economy with a 12-18 month lag. This indicator has already been warning us for quite some time of a slowing economy. Where are we now? The impact of rate hikes seems to trickle down a little faster than expected and we are starting to see a turning point in late 2023/early 2024. The economy is expected to continue to slow through December, but we are starting to see a distant light on the horizon.

Change in interest rates and ISM manufacturing index:

Fixed income:

For the first time since September 2019, supply chain pressures are in negative territory, meaning they are below the historical average. So the impact of supply on inflation has completely dissipated.

Pressure on the supply chain (USA):

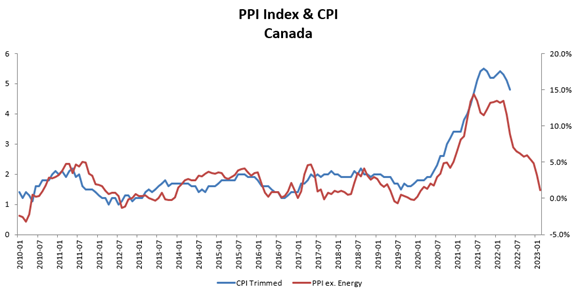

In Canada, the producer price index is a 9-month leading indicator of inflation (trimmed average). This index has fallen sharply and suggests a return to the top of the Bank of Canada range (about 3%) in the 4th quarter of 2023.

Producer price index and inflation (Canada):

In Canada, rates are expected to remain stable through the end of the summer and then decline in the third quarter. In the United States, the FED could opt for a final hike of 25 points in May, but with the current uncertainty, this is unlikely. Similar to Canada, rates could start lowering in the third quarter and continue into 2024.

Short-term interest rate (USA):

In Canada, it is easy to invest at rates of 4.5-5% taking very little risk. Canadian treasury bills offer around 4.5% for 3 months, while corporate bonds offer 5%.

Corporate Bond Interest Rates (Canada)

Stock markets:

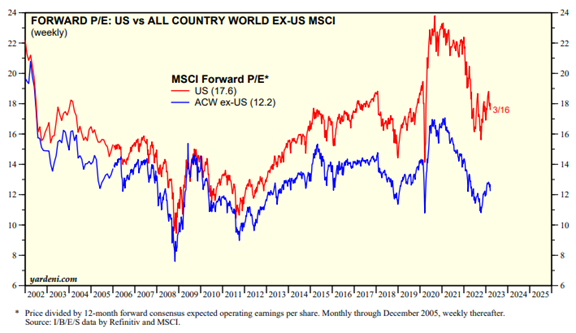

Since their peaks in mid-2021, stock market valuations have corrected sharply. The European/Asian and Canadian markets are now trading close to their historical averages of the past 20 years. In the United States, valuations are still high, but the concentration in high-growth technology stocks is skewing the comparisons somewhat upwards.

Stock Valuations: US and Europe/Asia

Stock valuations: Canada

However, ratings are not good indicators of short-term performance. They are the foundation of medium and long-term returns. We must continue to keep the focus on the cyclical data of the economy. The ISM manufacturing indices continue to record cycle lows. As the following graph shows, corporate profits will likely be revised downwards in the coming quarters.

ISM Manufacturing Index and Profit Growth:

If we look at the new orders data from the ISM survey, we come to the same conclusion. Company executives will steer analysts and investors toward lower earnings forecasts.

New orders and profit forecasts by companies:

In short, no clarification is visible by the end of 2023.

Finally, back to credit terms. Current conditions are historically highly correlated with stock market volatility. In other words, difficult access to credit is synonymous with a stock market correction.

Credit conditions and stock market volatility:

CONCLUSION :

The bear market is likely to continue with declining corporate profits and possibly a capitulation. Given the current uncertainty and the strong returns that can be generated in fixed income securities, the attractiveness of owning equities is weak.

Frédéric Mercier CFA, SIPC

Director – Financial markets