FINANCIAL MARKETS REVIEW

After an extraordinary month of November, the markets did it again in December, following the Fed’s pivot on their key rate. A big rate cut in 2024 is almost now official. We will come back to this. The American stock market returned 4.5%, while the S&P/TSX index rose 3.9%. Europe-Asia and emerging markets also made notable gains.

As for interest rates, they fell sharply in December, including a drop of 0.44% for the 10-year maturity. This allowed the Canadian bond index to increase by 3.2% (+7.3% over 2 months).

Economy :

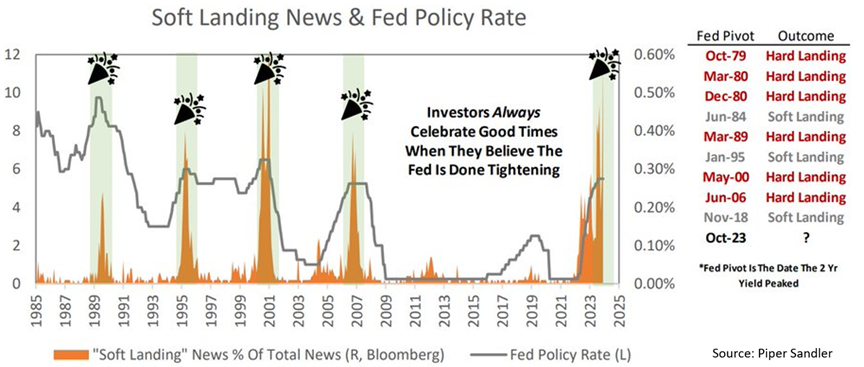

At its December meeting, the Federal Reserve revised its rate forecasts (pivot) sharply downward for 2024 and 2025. Rate cuts are now strongly telegraphed. As might be expected, the initial reaction was to celebrate the rate cut. This reaction is normal in the context, because historically, during monetary policy pivots, investors almost always believe that monetary authorities will achieve a soft landing and avoid a recession. Unfortunately, they are wrong ¾ of the time. The Fed’s pivots are often the peak of stock values. Remember that rate cuts generally occur when the economy is slowing down, which is far from good news for corporate profits.

Soft landing and Fed rates (US):

Although resilient in 2023, data relating to the job market continues to deteriorate little by little. Indeed, the Composite ISM Employment index is at the level of 2008 and 2020.

ISM Composite Employment and unemployment rate (United States):

During economic downturns, temporary jobs are the first to suffer. A significant contraction in temporary employees is a leading indicator of recessions. Unfortunately, as shown in the following graph, the contraction in temporary employment is now more than 9%.

Temporary jobs (United States):

Record debt combined with skyrocketing interest rates mean that household interest charges are now particularly high.

Interest payment as a % of income (US):

What partially saves the day in the United States is that sensitivity to mortgage rates is low, because many households opt for 30-year rates. It hurts less in the short term, but these impacts will be felt for a long time to come.

Average mortgage interest rate (United States):

Fixed income:

Like mortgage rates (USA), the cost of corporate debt does not yet reflect recent rate increases. The current cost of debt is significantly higher than that on corporate books. A lot of debt will mature in 2024 and 2025. Companies’ balance sheets (and profits) will be directly impacted by these increases in the cost of financing.

Corporate debt refinancing (United States):

In addition, credit conditions remain very restrictive. Banks are more cautious and restrict their loans and charge more when they do.

Credit terms and business loans (United States):

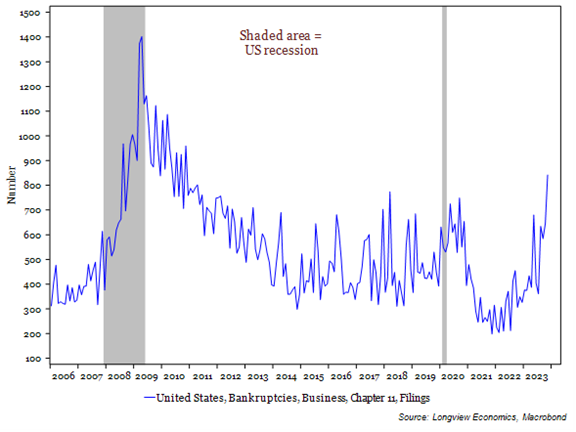

Business bankruptcies are already reaching levels reached in 2010. This number is expected to continue to rise in 2024.

Corporate bankruptcies (United States):

In terms of consumer prices, they should continue their slow decline. The core CPI should return to almost 3% around mid-year.

Leading indicator of inflation and CPI (United States):

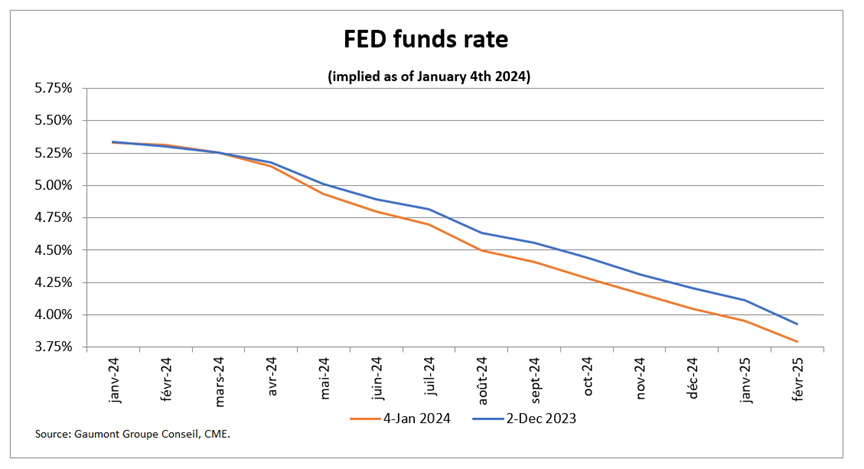

Finally, the reduction in the key rate in the United States is becoming more and more certain. In fact, a rate cut is anticipated at 92% for the May 1 meeting. Market operators now anticipate a rate of 4.05% at the end of 2024, a drop of 1.3%.

Implied short-term interest rates (United States):

Stock markets:

The American stock market ends the year with an increase of more than 14% in the last 2 months of the year and 26% for 2023. Following the Fed’s pivot on interest rates, the market has become euphoric in addition to being expensive.

Stock market euphoria and S&P 500 (United States):

One of the main elements behind this euphoria are the technological stocks which are referred to under the name Magnificient Seven (see the list below). These latter securities achieved a performance of 75% in 2023. These securities attract astronomical sums of investment. Investors believe these stocks are invincible. It’s reminiscent of the 2000s.

2023 stock market performance:

The growth expectations for these companies are so high that they are almost unattainable. The risk of disappointment and correction is high. These securities represent nearly 17% of the World index, the equivalent of the 5 largest countries (excluding the USA). It becomes a portfolio concentration problem.

Weighting of the Magnificient Seven and various countries in the World Index:

We can also see the euphoria in the following graph, where we see the American stock market rising sharply, while the outlook for economic growth is negative.

Conference Board leading indicator and S&P 500 (United States):

This weak economic outlook translates into forecasts of falling profits in 2024, but possibly growth in 2025.

Leading indicator of S&P 500 corporate profits (US):

CONCLUSION :

At the start of 2024, holding bonds looks favorable compared to stocks. High interest rates (in money markets and bonds) make it possible to generate an attractive return without taking too much risk. Investors are well paid to wait for opportunities to arise, possibly in the second half of the year.

Frédéric Mercier CFA, SIPC

Director – Financial markets