FINANCIAL MARKETS REVIEW

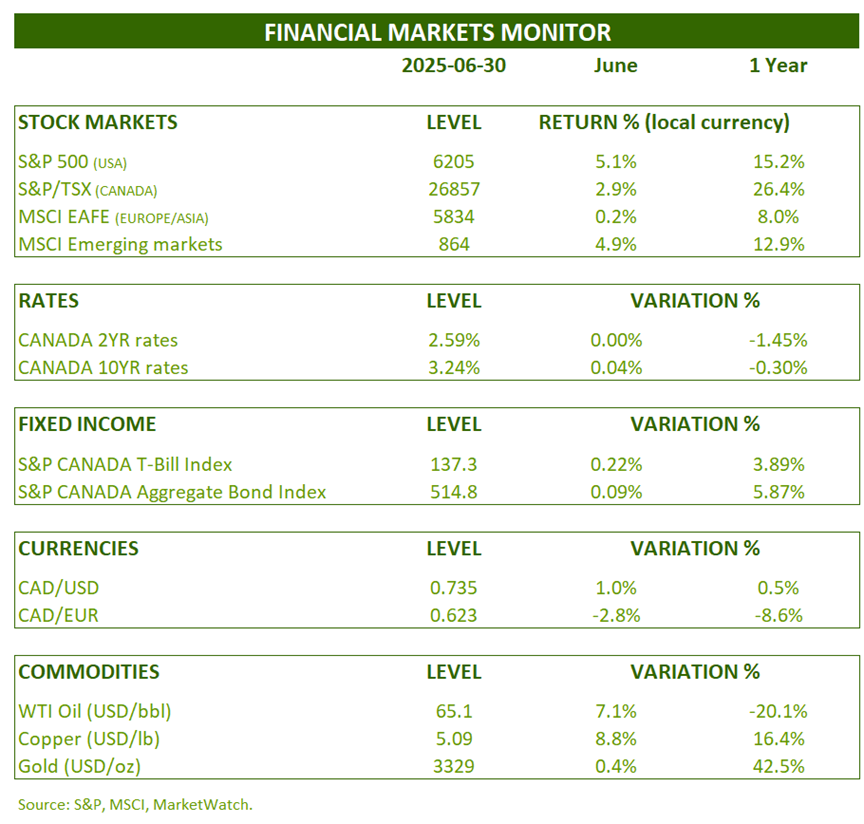

June was a very strong month for the stock market. The U.S. stock market generated a return of 5.1%, a 25% return from its low point shortly after Liberation Day. The Canadian stock market also performed well, returning 2.9%.

Emerging market stock markets generated a return of 4.9%. Regardless of the state of the economy and global conflicts, investors (primarily individual) are relentlessly buying stocks.

Interest rates were stable throughout the month. The Canadian bond index returned 0.09% in June and 5.87% over the past 12 months.

The US dollar continues to be under pressure against most currencies. In June, it lost 1% against the Canadian dollar and -2.75% against a basket of currencies.

OUTLOOK:

Economy:

After months of economic fear, investors seem to have put on rose-tinted glasses regarding the outlook and risks of the global economy.

The impact of tariffs will last for several quarters; it is too early to declare victory. The Iranian conflict could continue to put pressure on oil prices (which reached $78 for a few days in June). Uncertainty and risks remain high.

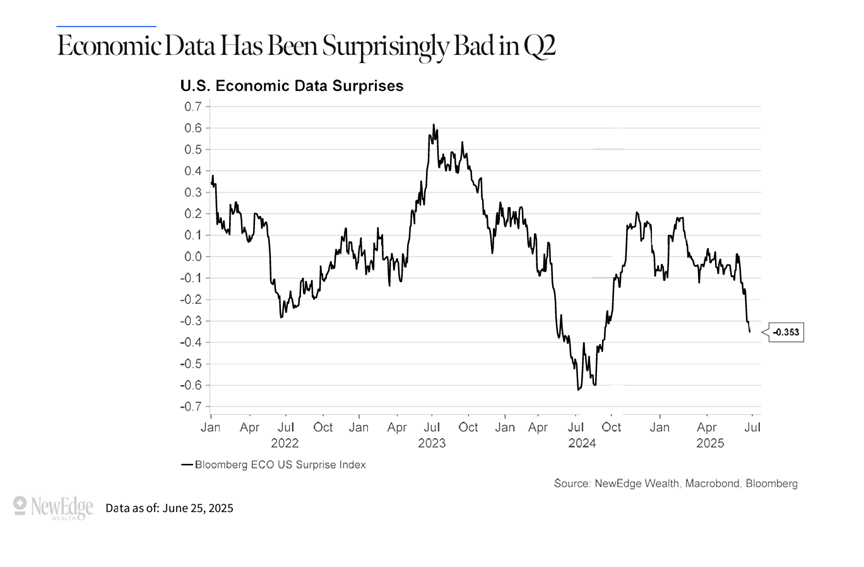

Yet, in the second quarter, economic data came in below those expected by economists, as shown in the following chart.

Economic Surprise Index (United States):

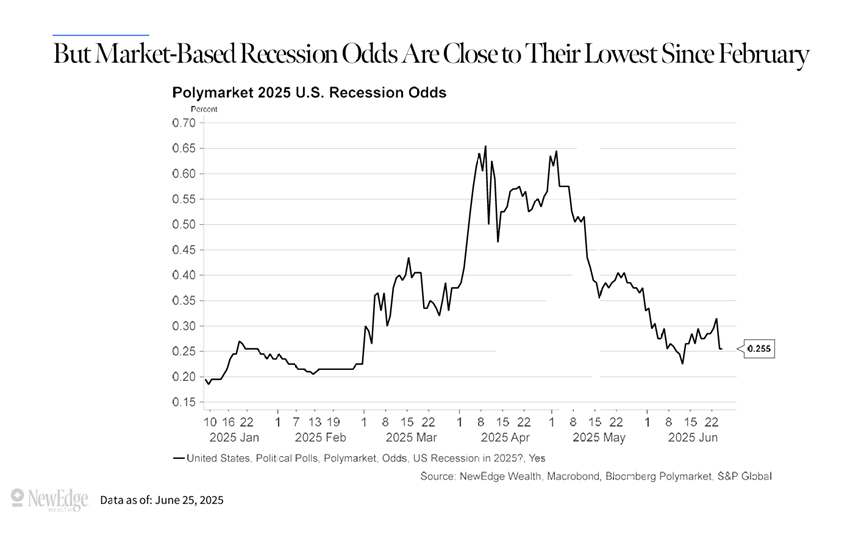

Moreover, even though consumption and GDP data have been stagnant for the past six months, the probability of a recession in 2025 has returned to its pre-tariff level.

Probability of a recession in 2025 according to the Polymarket website (United States):

The latest U.S. employment data show that job creation is continuing, but total hours worked are growing at anemic rates.

Total Hours Worked (U.S.):

In short, the economy remains growing, but investors seem to want to ignore the risks. Yet, President Trump has accustomed us to a great deal of volatility and uncertainty.

One asset that has been under pressure recently in the United States is the dollar. Indeed, since mid-January (the start of the tariff war), the dollar has lost more than 13%. Investors are shying away from the dollar for two main reasons. First, public finances are out of control. Second, the trade war is leading central banks to rethink their foreign exchange reserves. For example, they are selling US dollars to buy euros.

Evolution of the US dollar (against a basket of currencies):

This regime change appears to be the beginning of a weaker US dollar. Despite the recent decline, the US dollar remains fundamentally overvalued against most currencies. For example, the Canadian dollar is 14% undervalued. The equilibrium value is around 1.20.

Currency valuations against the US dollar based on purchasing power parity:

Fixed Income:

The housing component of inflation has been the factor that has slowed the decline in inflation for the past four years. However, month after month, the situation is improving. For the three months ending in May, the annualized change was 3.3%, exactly the pre-pandemic average.

CPI Housing Component: United States

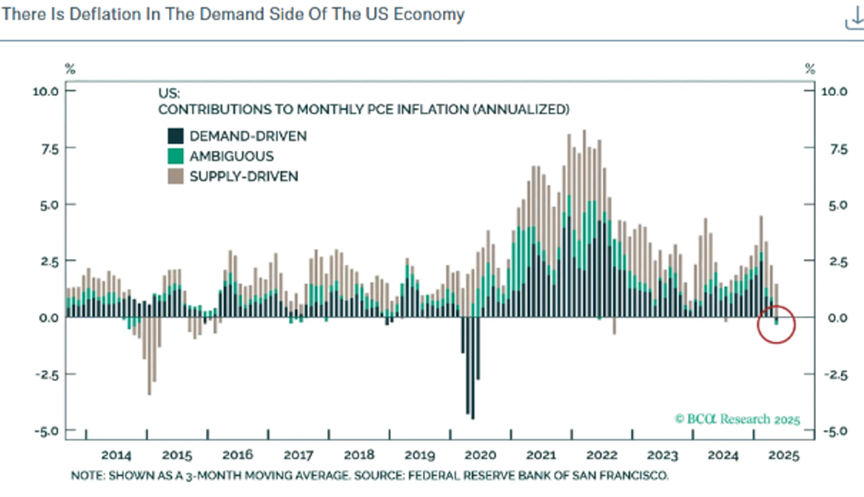

Every month, the San Francisco Federal Reserve analyzes inflation changes by component: demand-side and supply-side inflation. However, the most recent data shows that demand-side inflation is now in negative territory, a first since 2020. This indicates that the inflationary pressures the Fed can act on are practically zero. This gives Jerome Powell ammunition to lower the key rate, especially since Trump is putting pressure on him to do so.

Contribution of the various components of inflation: United States

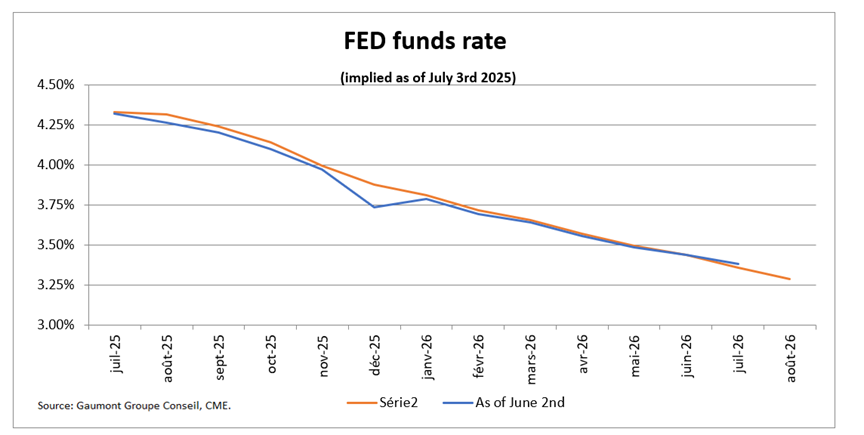

Expectations for Fed rate cuts remained stable in June. Market participants currently forecast a 0.45% cut in the federal funds rate in 2025 and a 0.90% cut in the next 12 months.

U.S. short-term implied interest rates:

Stock Markets:

Panic is now giving way to euphoria. Investors seem to be blinded and see no short-term risks.

Yet, it’s a safe bet that earnings will be revised downward in this trade war. One thing is certain: management and analysts’ visibility on earnings is not very good.

Earnings Revisions: MSCI World:

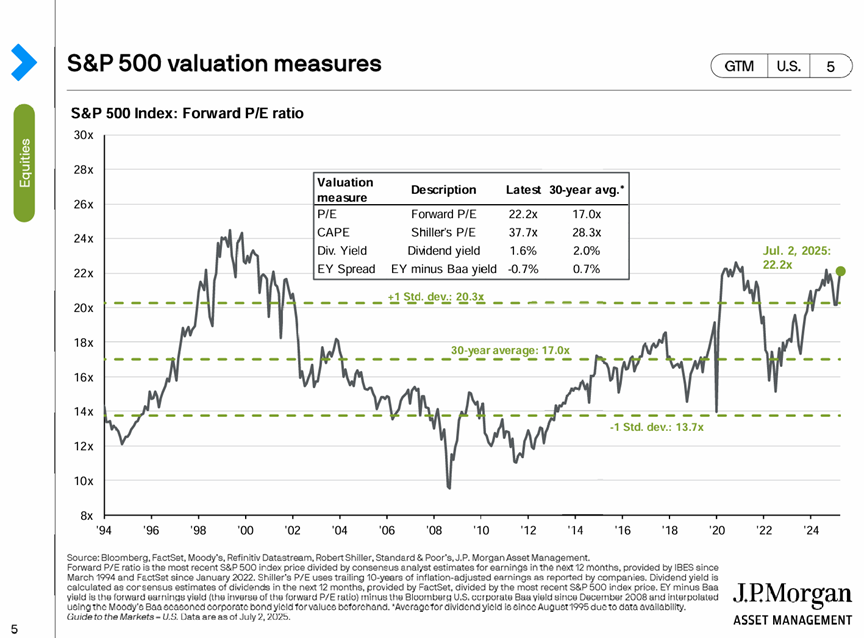

The S&P 500 Index is back at a high valuation from before the April panic and even the 2021 peak.

S&P 500 Price-to-Earnings Ratio:

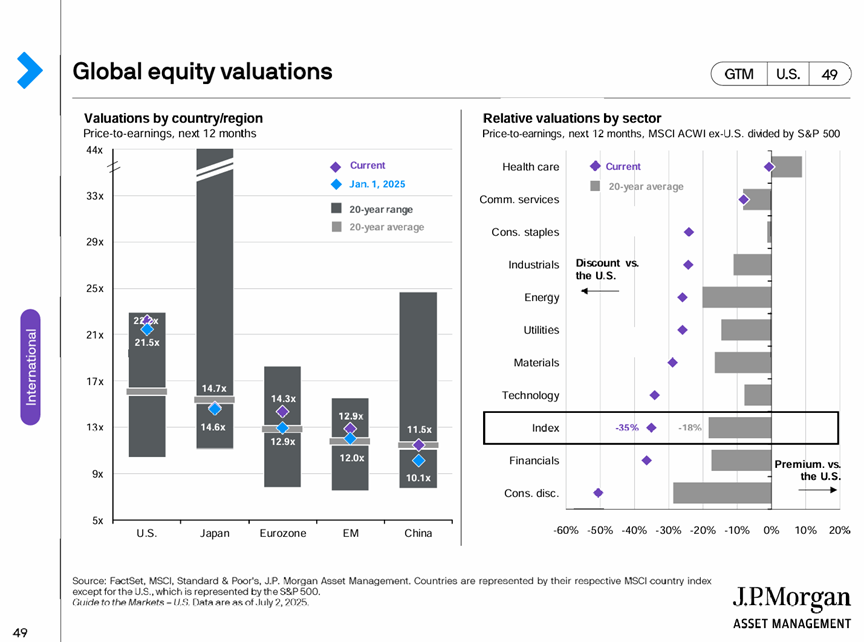

On an aggregate basis, and even by sector, US corporate stocks are much more expensive than those of other countries. Given similar growth, stock market valuations should converge, but this is not the case.

Global stock market assessment:

CONCLUSION :

The rebound over the past three months has been particularly robust. A period of consolidation is expected. Portfolio rebalancing is recommended. This will ensure profits are taken (and underperforming assets purchased) and a return to target. This will bring portfolio risk back to the original target level (risk tolerance). It is important to maintain well-diversified portfolios, both geographically and with fixed-income securities. Holding quality securities is more important than ever.

Frédéric Mercier CFA, SIPC

Director – Financial markets