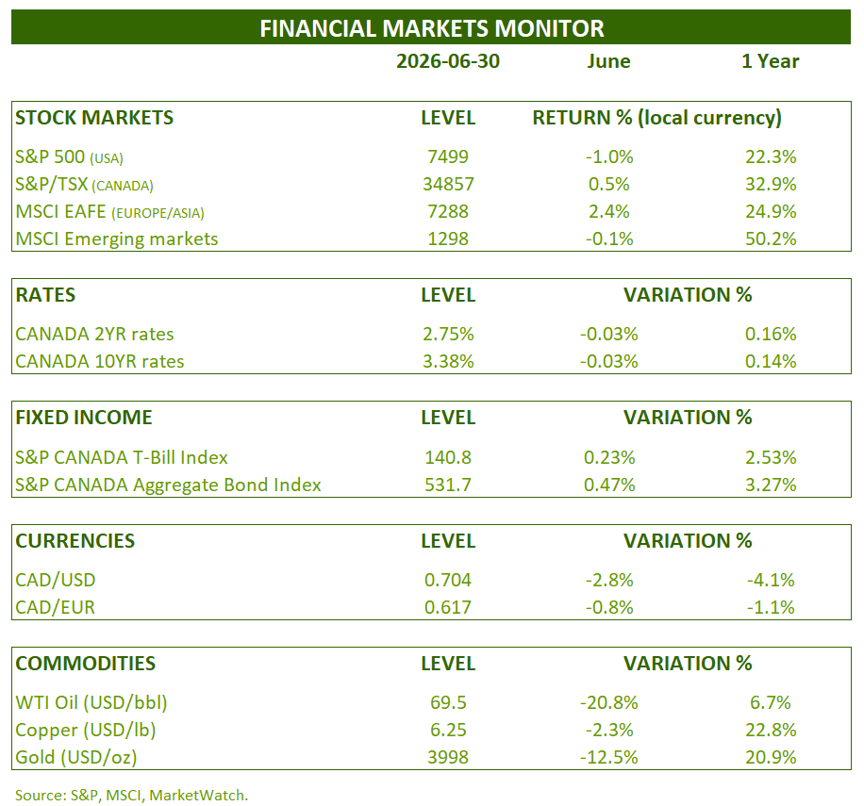

FINANCIAL MARKET REVIEW:

June was a highly volatile month for financial markets worldwide. The new Fed chairman appeared decidedly more restrictive than the Powell administration.

The US market edged down slightly by 1% during the month. High-momentum stocks, on the other hand, rose by 7.51%. The S&P/TSX Composite Index generated a return of 0.5%.

Interest rates remained relatively stable throughout the month. In fact, 2-year and 10-year maturities ended the month down by 0.03%.

As a result, the Canadian bond index rose 0.47% in June.

The sharp decline in oil prices (-20.8%) and gold prices (-12.5%) weighed heavily on the Canadian dollar. Indeed, it lost nearly 3% in June and is down 5% since its low in May.

OUTLOOK:

Economy:

We continue to closely monitor PMI indices worldwide. These all remain above 50, indicating growth in global industrial production.

Global Manufacturing PMI Indices:

At his first meeting, the Fed Chairman (Warsh) sought to outline his vision for monetary policy. The policy focus will be on price stability (2% target). Unemployment will become a secondary objective. The Fed’s communications will now be simpler and shorter.

In its forecasts, the Fed has shifted from a bias toward easing to one toward raising interest rates. Its core inflation forecasts have been revised upward.

Fed Projections June vs. March (United States):

The Fed has stated that it still considers inflation too high and is pointing toward rate hikes. Beyond the rhetoric, inflationary pressures appear to be easing. First, the price of oil has fallen by 35% since its peak in March. Furthermore, as the following chart shows, wage pressures are decreasing and are expected to continue to do so in the short term.

Wage Costs (United States):

In terms of employment, the market remains weakly growing. Nothing to give the Fed any ammunition, on either side.

Labor Market (United States):

On a medium-term note, a study published in June demonstrates that, contrary to popular belief, firms that invest the most in artificial intelligence see their employee numbers grow faster than those that invest little.

This is consistent with economic theory. The most productive companies generally grow faster, make more profit, and their employee numbers increase faster than less productive companies.

Artificial intelligence and jobs (United States):

Fixed income:

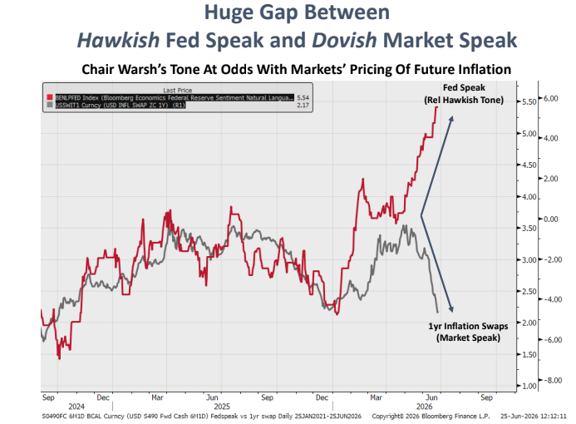

President Warsh’s bias toward rate hikes seems driven more by a desire to bolster his credibility than by fear of inflationary pressures. We can observe this dichotomy in the following chart. On the one hand, the Fed is using restrictive language, while inflation expectations for the next 12 months are falling to around 2%.

Fed bias and 1-year inflation swap (United States):

Furthermore, as expected inflation falls (assuming constant interest rates), real interest rates rise, making monetary policy more restrictive. The Fed doesn’t need to do anything, and monetary policy becomes restrictive on its own.

2-year real interest rates (United States):

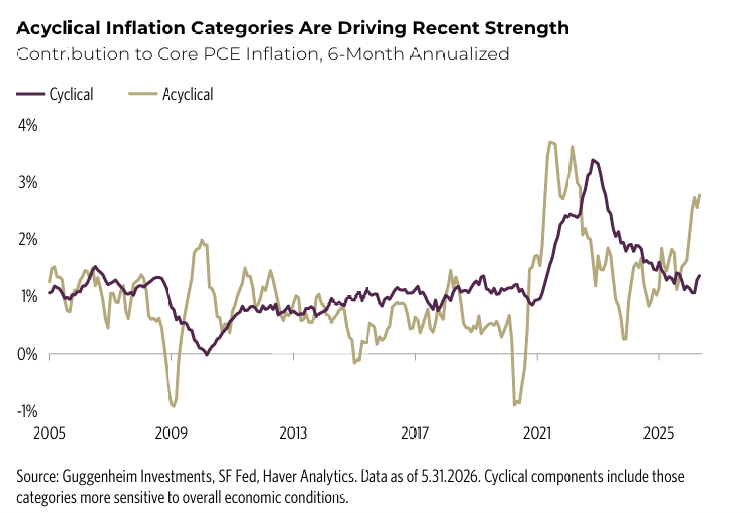

Ultimately, monetary policy is effective in countering overheating demand (cyclical) but not in addressing supply shocks or sectoral pressures (acyclical). However, cyclical pressures are currently contained. The recent rise in inflation is the result of acyclical pressures.

In short, the Fed Chairman shocked the markets, but his rate hikes are expected to be small or nonexistent.

Cyclical and acyclical inflation (United States):

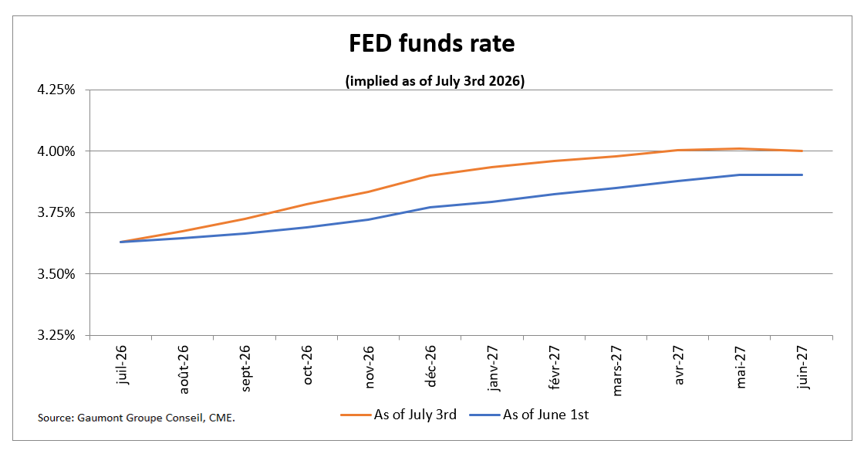

Expectations for the Fed’s key interest rate rose in June, as expected. A 0.27% increase is projected by the end of 2026 and another 0.10% in the first half of 2027.

In Canada, there is a 50/50 chance that the Bank will raise its key interest rate by 0.25% by the end of the year.

Short-term implied interest rates (United States):

Stock Markets:

The backdrop for global stock markets remains favorable. Earnings for the MSCI World Index continue to be revised significantly upwards. Stocks and sectors are moving less in correlation, which promotes diversification.

Forecast earnings growth for the MSCI World Index:

Unfortunately, when the stock market rises, some prioritize momentum over quality and profitability. This is illustrated in the following chart. Let’s look at the performance cycles of unprofitable technology stocks. This is a clear example of speculation.

Returns of Unprofitable Technology Stocks (United States):

The arrival of leveraged exchange-traded funds (ETFs) is fueling speculation. However, the amounts invested in these types of funds have doubled in the last year.

Value of leveraged exchange-traded funds (United States):

The four diversified tech giants (Google, Meta, Microsoft, and Amazon) are now trading at the same multiple as the S&P 500 as a whole! And this is despite their significantly higher profitability and growth.

Price-to-earnings ratio of the S&P 500 and the four diversified tech giants (United States)

CONCLUSION:

The correlation between stocks is at its lowest level in 10 years. This means that stock selection adds more value and macroeconomic factors are less important. It’s the perfect time to stock up on quality stocks when speculators only have eyes for high-momentum stocks.

Frédéric Mercier CFA, SIPC

Director – Financial Markets