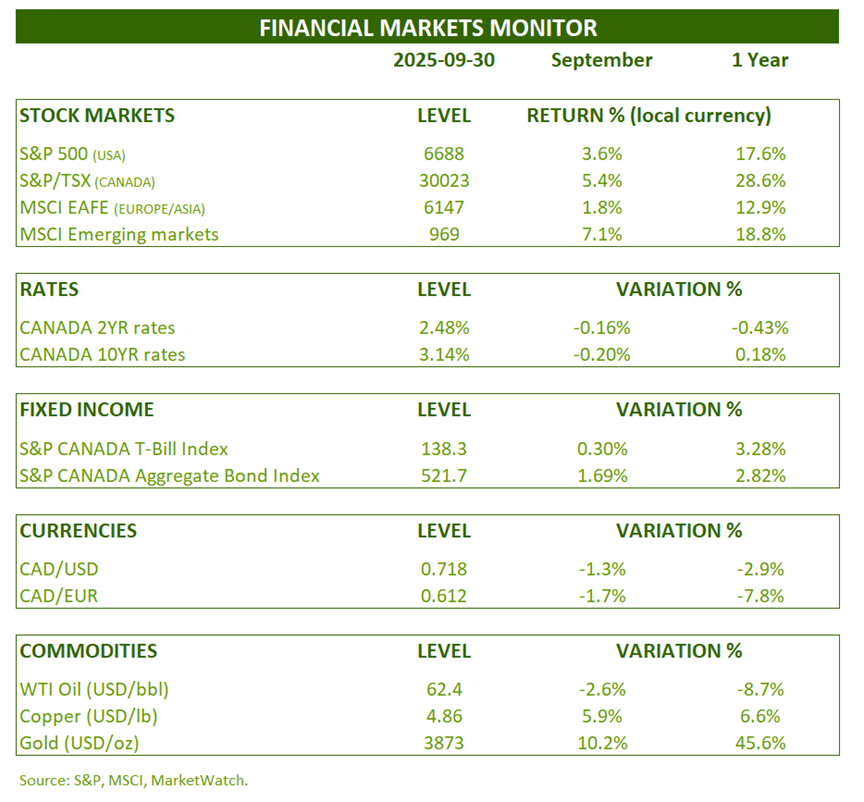

FINANCIAL MARKETS REVIEW

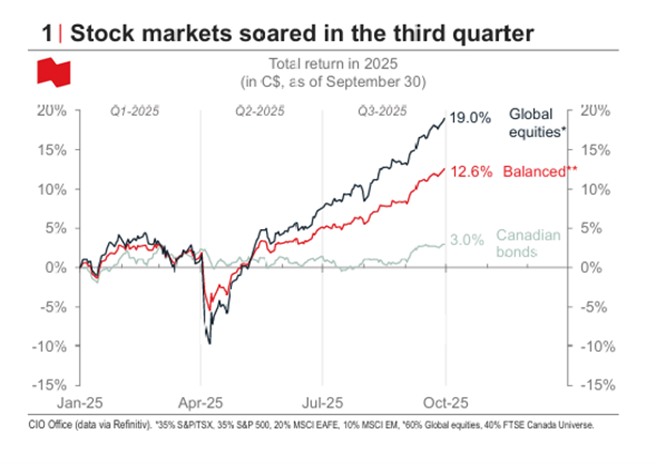

The third quarter of 2025 has just ended with a bang. Indeed, the Canadian stock market achieved a return of 5.4% in the month of September alone (11.8% for the three months). The US S&P 500 index also performed very well, gaining 3.6%. Emerging markets were not far behind, with a performance of 7.1%. Stock market growth was looking good in 2025, but exploded starting on August 21, when the Fed Governor signaled that the Fed would resume lowering its key interest rate. This was done on September 18.

As the following chart shows, 2025 has been an exceptional year so far.

Like the Fed, Canada lowered its key interest rate in September.

Canadian and U.S. interest rates fell during the month. The Canadian 10-year yield fell by 0.20%. As a result, the Canadian bond index returned a very strong performance in September, at 1.69%.

OUTLOOK:

Economy:

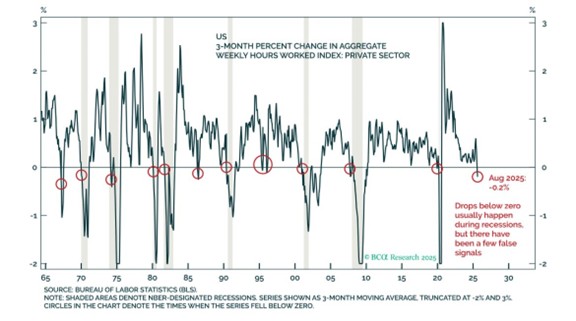

For four months now, job growth has been anemic in the United States. If we dig deeper and include hours worked, the situation is even worse. Indeed, total hours worked (as a three-month change) are negative. More often than not, negative growth implies a weak economy or one in recession.

Total hours worked per week in the private sector (United States):

One of the sectors affected is construction. Job openings (in %) are at their lowest level in 10 years. This is a direct reflection of the weakness in housing starts and real estate in general.

Job openings – construction (United States):

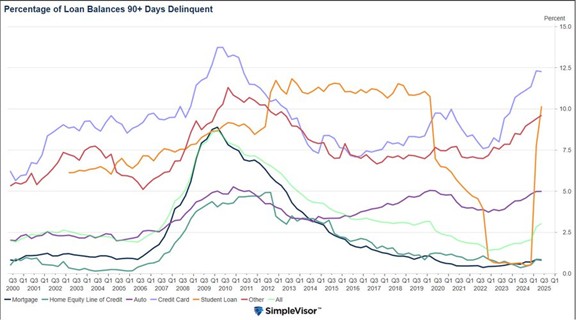

A weak job market often means higher defaults. This is even more true when interest rates don’t fall quickly. The Fed has only lowered its key interest rate by 0.25% in 2025. We can see that defaults are almost universally on the rise. Auto loans and credit cards have default rates comparable to those in 2009-2011.

Weak employment combined with high default rates gives the Fed ammunition to lower rates. This is less good news for corporate profits.

Default rates on various types of loans (United States):

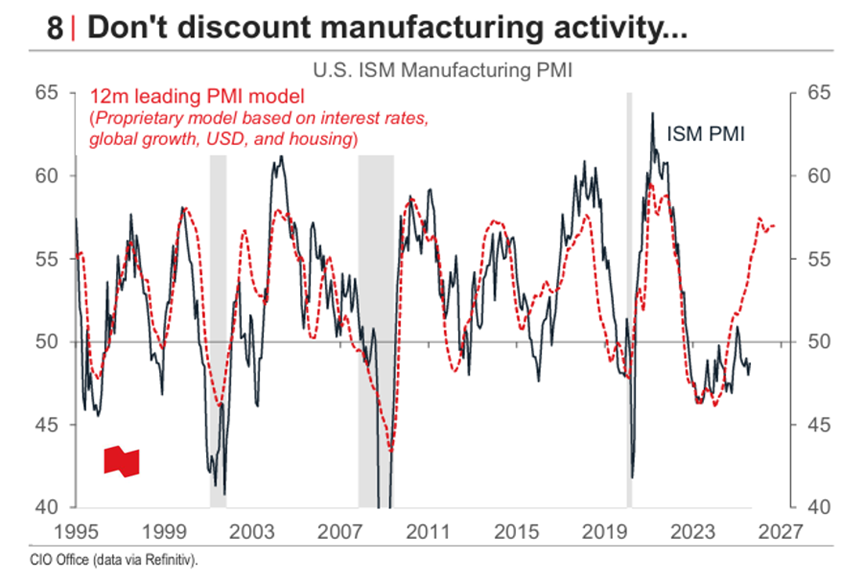

As we’ve long emphasized, the most important elements in analyzing the economic situation are leading indicators. Interest rate changes take time to impact the economy. The current weakness in the economy reflects past rate hikes. In the following chart, we see that the leading indicator projects attractive growth next year. It is, among other things, the rate cuts at the end of 2024 that are beginning to bear fruit.

Leading indicator of the ISM Manufacturing Index (United States):

Fixed Income:

After a recent rebound in inflation, likely due to tariffs, price growth appears to be on the decline. The NFIB Price Index has started to decline again, a six-month leading indicator of inflation.

NFIB Price and Inflation Index: United States

As we mentioned earlier, a weak job market allows the Fed to lower its key interest rate. When the job market is favorable, many workers quit to move elsewhere and earn higher wages. Therefore, the quit rate is directly linked to wage growth and even advanced by 12 months. What we’re seeing is that wage pressures will continue to weaken in the near future.

Quit Rate and Wage Growth: United States

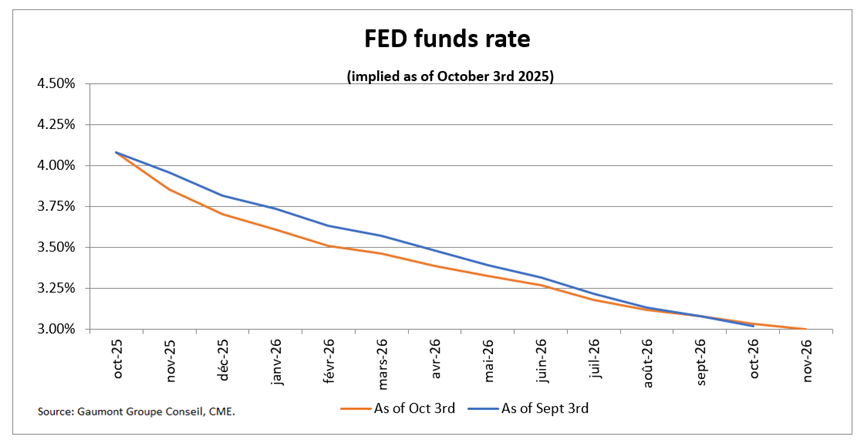

Expectations of Fed rate cuts have increased in recent months. Indeed, cuts of 0.38% are expected by December 2025 and 1.05% within 12 months.

Implied short-term interest rates (United States):

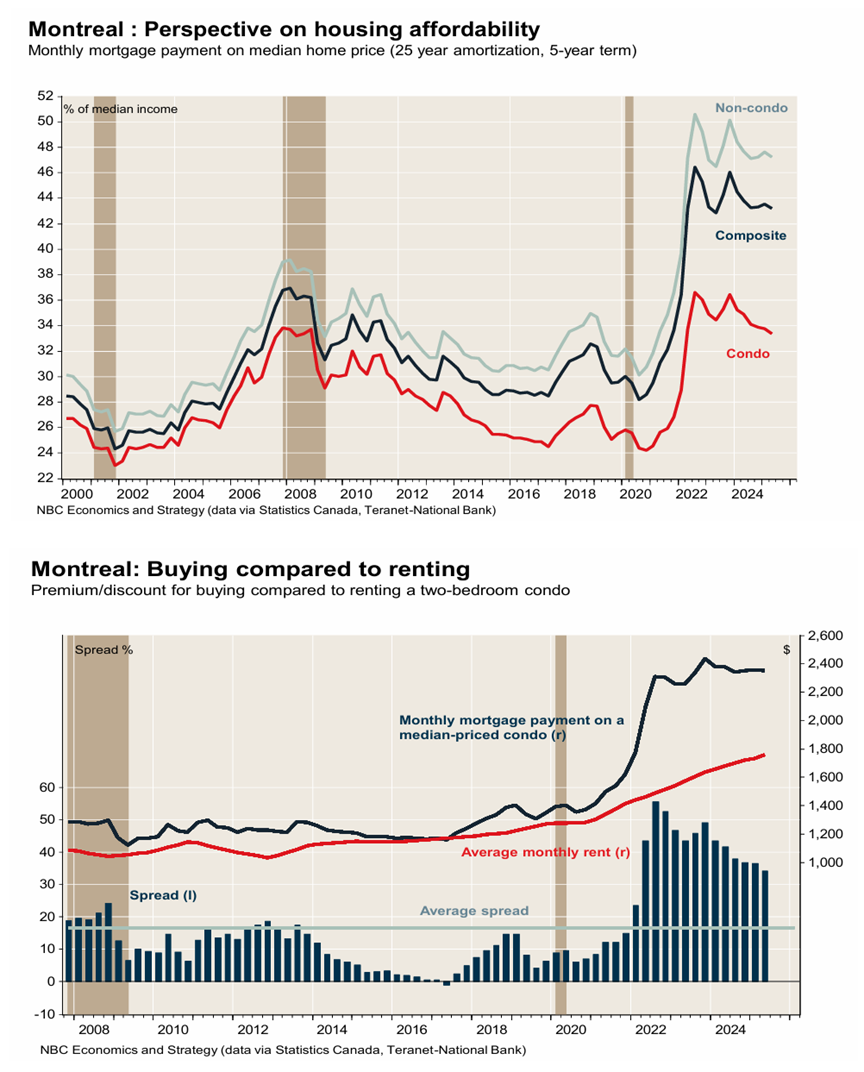

Finally, a quick word on the Montreal real estate market.

The percentage of median income devoted to mortgage payments continues to decline slightly, but remains much higher than during the pre-pandemic period. Price levels remain unsustainable in the long term. House prices cannot diverge from household income growth in the long term.

From another perspective, renting a condo is much less expensive than buying. In the long term, this situation cannot be sustained either.

Price adjustment will take several years.

Affordability of the Montreal real estate market:

Stock Markets:

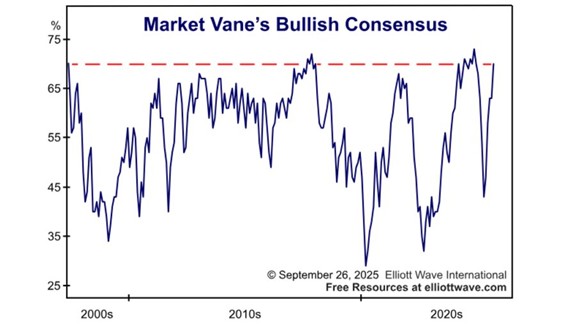

Despite the weakness of the job market, risks to the economic situation, and the very high valuation of indexes, the level of confidence among stock market investors is approaching euphoria. This doesn’t mean selling, but rather fastening one’s seatbelt tightly, as in the case of in-flight turbulence.

Stock market investor sentiment (United States):

At the same time, what are business leaders doing? They’re selling like there’s no tomorrow. This is another indicator that calls for caution.

Business leaders’ sell-to-buy ratio (United States):

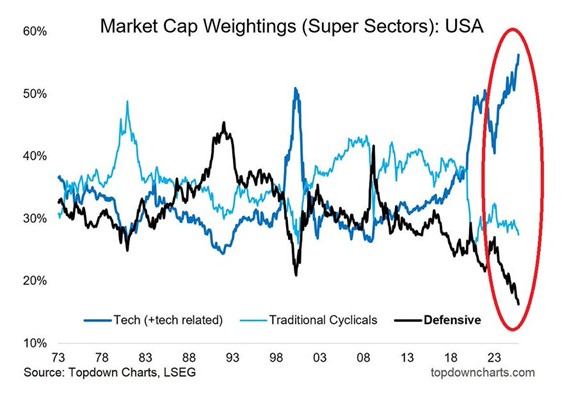

Over the long term, we see that the weighting of defensive stocks is at its lowest in 50 years. These stable (and often flat) stocks are often overlooked, among other things, in favor of more popular themes. There are certainly bargains to be found in these neglected, high-quality stocks.

Weightings of various segments of the stock market (United States):

CONCLUSION :

The year 2025 has delivered very good returns so far, but high valuations are expected to hamper future returns. This is the perfect time to thoroughly review your portfolio. It would be wise to bring your portfolio back on target. It is important to keep portfolios well diversified, both geographically and with fixed income securities. Holding quality securities at reasonable valuations is always the ultimate goal.

Frédéric Mercier CFA, SIPC

Director – Financial markets